Most buyers approach Miami with a budget in mind and a general idea of the area they want. What they rarely have is a clear picture of what their money actually buys once they start searching. And that gap, between expectation and market reality, is where most searches stall.

Finding an apartment for sale in Miami is not a single experience. It is four or five completely different markets stacked inside one city, each with its own inventory dynamics, buyer competition, financing rules, and timelines. A buyer at $350,000 in Kendall is navigating a different market from a buyer at $800,000 in Brickell, who in turn has almost nothing in common with someone shopping for miami penthouses for sale at $5 million in Miami Beach.

This guide breaks down what Miami real estate actually looks like across every major price tier in 2026, with specific data, honest trade-offs, and the market mechanics that determine whether you close at a good price or overpay. Before you search available Miami listings, read this.

Miami Is Not One Market, It Is Several, Stacked on Top of Each Other

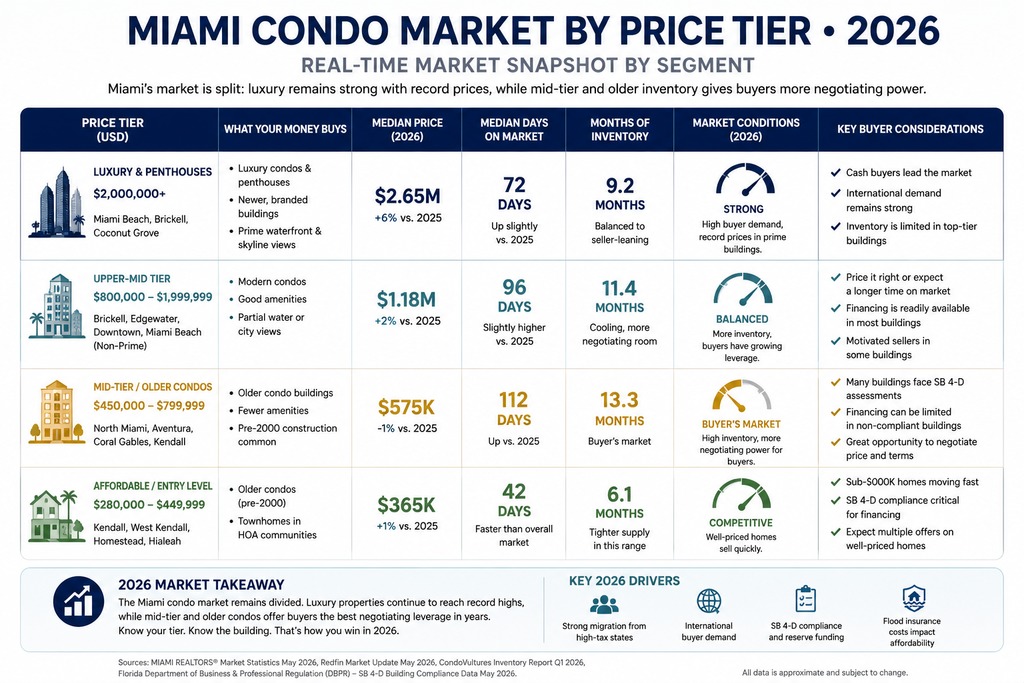

One of the most common mistakes buyers make is treating Miami-Dade data as a single number. When you read that the county median home price is around $575,000 or that average days on market is 96, those figures are averages across wildly different product types, price points, and zip codes. They mask as much as they reveal.

The real picture in 2026 is a bifurcated market. At the high end, luxury condos and Miami penthouses for sale in branded buildings along the Miami Beach waterfront and in Brickell are transacting at or near record prices, driven by cash-heavy buyers relocating from high-tax states and a strong international buyer pool. At the same time, mid-tier and older condo inventory in Miami-Dade is sitting with 13 or more months of supply, giving buyers in that segment meaningful negotiating leverage they have not had in years.

Single-family homes in the suburbs tell a third story. Inventory in areas like Kendall, Doral, and Homestead is up, but properties priced below $600,000 are moving faster than the overall statistics suggest, with median days on market in that sub-tier dropping to around 42 days as of April 2026.

So before you decide what to offer or how long to wait, you need to understand which tier of this market you are actually in. Here is what each level looks like right now. If you want to explore what is available in specific areas, the Brickell real estate guide, Doral listings, and homes in Kendall are good starting points.

What Affordable Homes in Miami Actually Look Like Right Now

The phrase "affordable homes in Miami" generates a lot of searches and a lot of disappointment when buyers realize what it means on the ground. At the $280,000 to $450,000 range, you are primarily looking at two types of product: older condos in buildings constructed before 2000, and townhomes in HOA communities in West Kendall, Homestead, or parts of Hialeah.

The Trade-Offs at Entry Level

Older condos in this price range come with a risk that did not exist five years ago at the same scale: Florida Senate Bill 4-D, passed after the Surfside collapse, requires buildings over 30 years old to complete structural inspections and fund reserves. Many pre-2000 buildings are now passing those costs along as special assessments, which can run anywhere from $28,000 to $75,000 per unit. Some are financed over time through higher monthly HOA fees; others require a lump-sum payment at or after closing.

For financed buyers, this creates a practical problem: FHA and conventional loans through Fannie Mae will not approve purchases in condo buildings that are not SB 4-D compliant. If you are using financing rather than cash, a pre-2000 building carries real closing risk. The hidden costs every Miami buyer needs to know include more than just closing fees, reserve assessment exposure can add tens of thousands to the real cost of an older unit.

Townhomes in West Kendall and Homestead offer a different entry point. The product is newer, the buildings are SB 4-D compliant, and in some communities you can find three- and four-bedroom homes with garages for under $450,000. The trade-off is commute time and distance from Miami's core employment centers.

Where the Real Opportunity Is in 2026

The highest leverage in the affordable segment right now is in post-2000 condos in the $350,000 to $480,000 range, particularly in areas like North Miami Beach, parts of Doral, and along the Kendall corridor. These buildings cleared the structural inspection threshold with no outstanding assessments, qualify for conventional financing, and in some cases are sitting in a supply-heavy environment that has given buyers pricing power they have not had since 2020.

For first-time buyers working through this segment, there is also a layer of program options worth knowing. Down payment assistance programs, FHA loans with as little as 3.5% down, and certain Florida Housing Finance Corporation products are all in play at this price tier. The first-time buyer advice for Miami covers how to structure that search.

The Mid-Market Sweet Spot, and Why It Moves Fast in Certain Pockets

The $500,000 to $1.2 million range is the highest-volume segment in Miami-Dade real estate by transaction count. It spans a wide band of product: two, and three-bedroom condos in Brickell and Edgewater, townhomes in Doral and Palmetto Bay, and single-family homes in Kendall, South Miami, and Coconut Grove.

The volume is not evenly distributed. Townhomes are currently the fastest-appreciating product type in Miami at 12.4% year-over-year, driven by buyers who want more space than a condo offers but cannot access the single-family market without stretching their budget. A well-priced townhome in a desirable HOA community, listed at $650,000 to $750,000, routinely generates multiple offers within the first ten days.

A Real Example: Doral, 2025

A three-bedroom, two-and-a-half-bath townhome in a Doral gated community was listed at $689,000 in late 2025. The unit had been updated, was in a post-2015 building with low HOA and no pending assessments, and was priced at roughly $375 per square foot, slightly below comparable sales in the submarket. It received four offers in the first weekend, went under contract at $712,000, and closed in 38 days. The buyer used conventional financing with 20% down.

That outcome is not unusual in the Doral sub-$800,000 single-family and townhome segment. What makes Doral specifically attractive is the combination of school ratings, newer construction, lower insurance rates relative to coastal properties, and an inventory level that stays tight because demand from Venezuelan and Colombian buyers has remained consistent even as broader Miami condo inventory expanded.

Where Mid-Market Buyers Lose Leverage

The common mistake in this range is waiting. Buyers who spend three or four months gathering information, getting pre-approved slowly, or making low offers on well-priced listings repeatedly find themselves back at the beginning. In the sub-$800,000 single-family and townhome segment, a correctly priced listing in move-in condition does not need to negotiate. By the time a hesitant buyer circles back, the property is under contract.

In the Brickell condo tier at similar price points, the dynamic is different. A one-bedroom at $500,000 to $600,000 in an established building currently competes in a market with around 113 days on market and over 13 months of supply countywide. That is a buyer's market for condos, and it means you have room to negotiate. Use it. To see what is currently available, run the numbers on a mortgage before committing to a search range.

Miami Penthouses for Sale and the Luxury Tier, How This Market Operates

The $2 million-and-above segment in Miami, particularly Miami penthouses for sale and the most expensive homes in Miami, does not follow the rules that apply to the rest of the market. Understanding why makes you a significantly better buyer or evaluator of this segment.

Price Records and What They Actually Signal

In November 2025, a penthouse at Seaway at the Surf Club closed for $86 million, resetting Miami-Dade's condo sales record. At the ultra-luxury end, the Rivage Bal Harbour penthouse is listed at $150 million with 12,603 square feet of interior space. The Brickell mainland market set its own record with a Mandarin Oriental Residences penthouse closing near $49.9 million at approximately $6,300 per square foot.

These numbers are meaningful not because most buyers are in that range, but because they set the psychological floor for the tier just below. When $6,300 per square foot is the mainland ceiling, branded new-construction at $2,000 to $3,000 per square foot feels reasonable to the buyer who has been comparing across the top of the market. The anchoring effect is real and intentional.

How the Luxury Buyer Pool Works

The most important structural fact about luxury homes in Miami is the cash composition. In Q1 2026, mainland Miami luxury condo sales rose 13% year-over-year, with average prices up 18%. The buyer pool driving that growth is predominantly cash buyers: high-net-worth individuals relocating from New York, California, and New Jersey who are motivated by Florida's lack of state income tax, and a growing share of international buyers from Latin America, Europe, and Canada for whom Miami real estate functions as both a residence and a dollar-denominated asset.

For a cash buyer, the transaction mechanics are different. There is no appraisal contingency, no financing condition, and no lender-required condo approval process. Closing timelines can compress to three to four weeks when both sides are motivated. For a financed buyer entering this segment, understanding that your offer competes against cash on a regular basis is critical to structuring correctly.

Condo Association Vetting at the Top

Miami Beach condo buildings at the luxury level run their own approval processes that can add four to eight weeks to a closing timeline. Some buildings at Star Island, Fisher Island, and the top-tier Bal Harbour towers require board interviews, financial disclosures, and background reviews. Some have rental restrictions that affect the unit's income potential if you plan to use it part-time. The Miami Beach condo guide breaks down what to verify before making an offer in that market.

One practical nuance: list price at the top of the market is rarely the closing price, and not always because of discounting. Trophy penthouses sometimes close above ask when multiple qualified buyers are competing in the same window. The published average DOM of 137 days for Miami penthouses masks wide variance, some units sit for over a year, and others are absorbed in days through off-market channels before they ever hit MLS.

The Miami-Specific Variables That Affect Every Buyer Regardless of Budget

Whatever price tier you are searching in, there are four Miami-specific factors that shape your timeline, your financing options, and your total cost of ownership. These do not show up in the listing price, and they are where deals quietly fall apart.

Insurance

Florida's property insurance market has been contracting for years, and Miami-Dade is at the center of it. Coastal and older properties carry the highest premiums. A condo in a pre-2000 building in Miami Beach or Edgewater can generate annual insurance costs for the building itself that translate into HOA fees of $1,200 to $2,500 per month for a standard two-bedroom unit. Single-family buyers inland in areas like Kendall or Homestead see significantly lower rates, which is one reason affordability in those zip codes stretches further than the sale price alone suggests.

For buyers using financing, lenders will require proof of adequate coverage before closing. In some cases, the only available insurer is Citizens, Florida's state-backed insurer of last resort, which has its own coverage limits. Understanding insurance costs before you make an offer is not optional, it affects your monthly payment calculation and your ability to close.

The Surfside Legislation Effect on Older Condo Buildings

Post-2000 condos in Miami-Dade now have a structural market advantage over older buildings. Florida's SB 4-D legislation requires milestone inspections and fully funded reserves for buildings 30 years and older. Buildings that completed these requirements are marketing it as a selling point. Buildings that have not are seeing prices soften and days on market extend as buyers and lenders become more cautious.

The practical split: a pre-2000 condo with a pending or recent special assessment can represent genuine value for a cash buyer who factors that cost into the offer price. For a financed buyer, the same unit may be unlendable. Knowing which category a building falls into before you fall in love with a unit saves weeks of wasted due diligence.

Seasonal Demand Patterns

Miami real estate has a real season, and it affects negotiating leverage. Inventory typically peaks between October and February, when snowbirds are in town, Latin American buyers travel up during holiday periods, and competition from domestic relocators is highest. Listings that enter the market in November through January often receive stronger early offers.

The summer months, June through August, are historically the slowest period for Miami showings. Buyers who search during that window often find sellers more motivated, longer days on market on listings that did not move in season, and more room to negotiate. If your timeline is flexible, summer closings in Miami have quietly produced some of the most favorable buyer outcomes of recent years.

Foreign Buyers and Negotiation Style

Miami retains its position as the top U.S. destination for foreign real estate capital, with 42% of condo sales in Q1 2026 going to non-U.S. buyers. Lead source countries are Argentina, Colombia, Mexico, Brazil, and Canada. This buyer pool affects how sellers price and how quickly they respond to offers.

Foreign buyers in the $500,000 to $2 million range frequently pay cash at or near ask, do not request repairs, and can close in 30 days. A domestic buyer competing in the same range with a financed offer needs to compensate elsewhere, a larger earnest deposit, a faster inspection period, or a pre-approval from a lender the listing agent recognizes. Presenting your offer correctly in a competitive situation is not about being aggressive. It is about being organized and credible.

How to Search Miami Real Estate Without Burning Six Months

The buyers who move efficiently through the Miami market share one common characteristic: they aligned their financing, their search criteria, and their decision-making process before they started touring. The ones who struggle did it in the wrong order.

Most buyers start with Zillow or Realtor.com, fall in love with a listing, then begin figuring out financing. By the time they have a pre-approval in hand, the unit is gone. In Miami's faster-moving segments, a well-priced listing in sub-$800,000 single-family or townhome product can be under contract within a week of hitting MLS.

What MLS Data Does Not Show You

The publicly visible listing data shows price, photos, square footage, and HOA. It does not show you the building's reserve study, pending litigation against the HOA, the status of any structural inspection reports, the percentage of units rented versus owner-occupied (which affects conventional financing eligibility), or whether a special assessment vote is scheduled for the next board meeting.

These details determine whether a deal closes cleanly or falls apart at the financing stage. Getting them requires asking the right questions before going under contract, not after.

The One-Roof Advantage

Miami real estate transactions involve three separate professional services: the real estate transaction itself, the mortgage, and the title closing. Most buyers manage these with three separate companies that have never worked together before. Scheduling conflicts, communication gaps, and last-minute surprises in the financing or title work are the most common reasons closings get delayed or fall apart.

Working with a broker who also holds a mortgage broker license and a title agency means the same person managing your offer strategy is also coordinating your loan and clearing title. The timeline compresses. Problems surface earlier, when they can still be solved. For buyers comparing how to start your Miami home search, that structural difference in how the transaction is managed affects both the experience and the outcome.

Frequently Asked Questions

Q: What is a realistic monthly budget for an apartment for sale in Miami once you include HOA fees?

A: The sale price is only part of the equation. A $450,000 condo in a full-service building in Brickell or Edgewater can carry HOA fees of $800 to $1,400 per month, which adds roughly $10,000 to $17,000 per year to your ownership cost before taxes and insurance. At the affordable end of the market, older buildings in Miami-Dade sometimes run lower HOA fees but compensate with higher insurance costs passed through the association. A practical rule for budgeting in Miami: calculate your all-in monthly cost using the actual HOA, your estimated insurance contribution, and your mortgage payment together. Many buyers discover their real purchase ceiling is $50,000 to $80,000 lower than their initial pre-approval because of this.

Q: Are there still affordable homes in Miami for first-time buyers, or has that window closed?

A: The window is narrow but it has not closed. Affordable homes in Miami at the $300,000 to $480,000 range exist in West Kendall, parts of Hialeah, Homestead, and in post-2000 condo buildings that cleared the SB 4-D inspection threshold. The issue for first-time buyers is not that the properties do not exist, it is that the ones worth buying go quickly. A three-bedroom townhome in a Kendall gated community priced at $420,000 with no pending assessments and good school access will attract multiple offers. The buyers who compete successfully in that range are pre-approved, understand what they are looking for, and are ready to move within 48 to 72 hours of a suitable listing appearing.

Q: How are prices at the most expensive homes in Miami holding up compared to last year?

A: The most expensive homes in Miami and the top penthouse segment are performing stronger than the rest of the market. Mainland luxury condo sales rose 13% year-over-year in Q1 2026, with average prices up 18% in that same period. Miami-Dade's condo sales record was reset in November 2025 when a Surf Club penthouse closed at $86 million. The driver is a combination of wealth migration from high-tax states, strong Latin American and European demand, and a structural shortage of trophy product. At the ultra-luxury level, supply is genuinely limited, and that supports pricing even in a market where mid-tier condos carry over 13 months of inventory.

Q: What should I verify before touring miami penthouses for sale in a building with rental restrictions?

A: Four things, in order. First, confirm the percentage of units currently rented versus owner-occupied, buildings with more than 35% investor-owned units often cannot qualify for conventional or FHA financing on future resale, which limits your buyer pool when you sell. Second, ask for the most recent reserve study and any pending special assessments. Luxury buildings are not immune to deferred maintenance costs. Third, review the rental restriction policy in detail, some buildings cap rentals at 12 months minimum, others prohibit short-term rentals entirely, and a few allow 30-day minimums with restrictions. Fourth, confirm the board approval timeline. Some premium Miami Beach towers run approval processes of six to ten weeks, which must be factored into your closing date.

Q: How long does it typically take to close on a Miami condo once an offer is accepted?

A: For a cash transaction in a building with no pending approval process, 21 to 30 days is achievable. For a financed purchase in a standard resale condo, 35 to 45 days is realistic if the building is already approved by the lender. The timeline extends when the building requires a condo questionnaire review, when the lender has not previously approved that specific building, or when the HOA requires board approval for new buyers. Buildings in the luxury tier, particularly in Miami Beach zip codes, can add four to eight weeks if a board interview is required. The buyers who close fastest are those who start the lender's condo approval process at the same time they begin their search, not after an offer is accepted.

Ready to Search With a Clear Picture of the Market?

If you want to know exactly what is available at your price point right now, what the real carrying costs look like, and whether the building you are considering has any structural or financing flags, start your Miami home search here. Alberto Labrada handles the real estate, the financing, and the title, so instead of managing three separate professionals through a 45-day closing, you work with one person who sees the whole transaction.

Check out this article next