Most Miami-Dade homeowners think about home improvements in one of two ways: as a pre-listing move or as a personal preference. Both frames miss a third option that has quietly built real wealth in this market. Strategic homeowners are using accumulated equity to fund top home improvements that deliver measurable returns, generate federal tax credits, and reduce capital gains exposure at the same time.

The question is not whether to improve your home. The question is which improvements justify the investment, how to finance them without eroding your net worth, and what the IRS actually allows you to capture at tax time. Miami-Dade homeowners who get all three answers right are not just maintaining their properties. They are building equity systematically while reducing their eventual tax liability at sale.

This article gives you the framework to do exactly that.

Why Miami Homeowners Are in a Unique Position to Fund Top Home Improvements Right Now

Home values across Miami-Dade have climbed significantly since 2020. In Kendall, Doral, and Coral Gables alike, homeowners who purchased before 2022 are sitting on equity positions that were essentially unimaginable five years ago. A home bought in 2018 for $420,000 in Westchester may carry $550,000 to $580,000 in current market value. The spread between what you owe and what your home is worth is the resource most Miami homeowners are underusing.

Nationally, homeowners drew heavily on their equity during the low-rate era. Many Miami-Dade homeowners did not. With current home equity levels at or near record highs locally, and with a renovation market that rewards targeted upgrades differently than the national average, the calculus for funding improvements through equity looks different here.

Two Miami-specific dynamics make this moment particularly relevant. First, insurance costs in South Florida have reset buyer expectations: homes with impact windows, newer roofs, and updated electrical systems attract larger qualified buyer pools than those without. Homeowners who make those upgrades now are not just improving their living conditions. They are actively shaping their future sale outcome. Second, the equity available to most Miami-Dade homeowners right now often exceeds the total cost of the upgrades most likely to produce returns at resale. The capital is there. The question is how to deploy it intelligently.

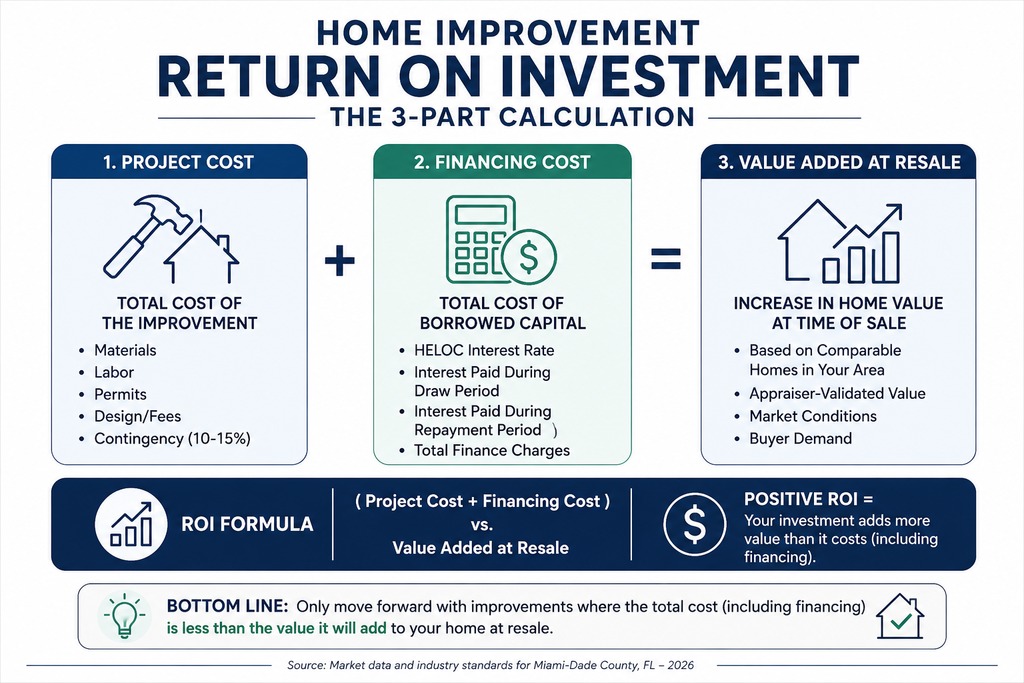

The Home Improvement Return on Investment Calculation You Should Run Before Spending a Dollar

Most homeowners calculate home improvement return on investment by subtracting what a project costs from what it adds to resale value. Accurate as far as it goes, but incomplete when financing is involved.

A complete home improvement return on investment calculation has three components: the cost of the project itself, the cost of the borrowed capital (interest paid on a HELOC during the draw and repayment period), and the value added at resale relative to comparable homes in your specific zip code. Leave the middle number out and you will overpay for upgrades that look profitable on paper but fall short once debt service is factored in.

Here is a concrete example. A homeowner installs impact windows for $20,000 financed through a home equity line at 8.5 percent over five years. Total interest paid: roughly $4,700. Total cost of the improvement including financing: approximately $24,700. If comparable homes without impact windows are selling at a $25,000 to $30,000 discount in that area, the upgrade still clears the bar with margin. Run the same math on a $55,000 kitchen gut renovation producing $28,000 in resale value and the answer is immediate: skip it.

For a detailed breakdown of which specific upgrades produce the strongest resale returns in Miami-Dade, this guide to home improvements that add value before you list covers the full project-by-project analysis. The goal here is not to repeat that list. It is to add the financing-cost layer that changes how you evaluate every item on it.

How a Home Equity Line of Credit for Home Improvements Works in Miami-Dade

A home equity line of credit for home improvements is a revolving credit facility secured by the equity in your property. Unlike a home equity loan, which delivers a lump sum at a fixed rate, a HELOC works more like a credit card tied to your home's value. You draw what you need, repay it, and draw again during the draw period, which typically runs five to ten years. After that, the line moves into repayment mode and the balance amortizes over the remaining term.

Lenders calculate your available line based on the current appraised value of your home minus what you owe, with most limiting total borrowing to 80 to 85 percent of the appraised value. On a Miami-Dade home worth $600,000 with a $320,000 mortgage balance, an 80 percent LTV ceiling gives you a maximum HELOC of $160,000. Most homeowners draw a fraction of that limit.

A few Miami-specific notes worth knowing before you apply:

Condo owners face a different path than single-family homeowners. Many lenders restrict HELOC availability on condominium units with high investor concentration or pending HOA litigation. If your home is a condo in Brickell or Coconut Grove, confirm lender eligibility before building a renovation plan around HELOC access.

HELOC rates are variable and tied to the prime rate. In the current environment, that means rates are elevated compared to 2020 and 2021. Modeling your monthly cost at various draw amounts before committing to a project scope is basic planning that most homeowners skip. The mortgage calculator on this site lets you do that in a few minutes.

Alberto Labrada holds both a Florida real estate broker license and a mortgage broker license. When a homeowner at Labrada Realty works through whether a home equity line of credit for home improvements makes sense given their equity position and renovation goals, the conversation stays in one place. The financing and the real estate outcome get evaluated together, without needing to loop in a separate lender for the strategic piece. Most agents refer you out for that conversation. This one does not.

The Consumer Financial Protection Bureau provides a plain-English explanation of how HELOCs work that is worth reviewing before you apply.

Top Home Improvements That Justify Borrowing Against Your Equity

Not every upgrade on the high-ROI list justifies financing. When interest cost gets added to the project total, the margin on weak-returning upgrades disappears fast. These are the top home improvements in Miami-Dade where the financing math still works:

Impact windows and doors remain the clearest case for HELOC financing. A full-home package runs $15,000 to $25,000 depending on the number of openings. In most Miami-Dade zip codes, the resale premium for impact protection is $20,000 to $30,000. The insurance savings, typically $2,000 to $6,000 annually, begin the day installation is complete. A Kendall homeowner near US-1 who financed impact windows through a HELOC is recovering part of the interest cost through annual insurance savings while the equity built into the upgrade compounds over time. Of all the top home improvements available to South Florida homeowners, this category has the clearest argument for debt-financing.

Roof replacement is worth financing when the current roof is generating buyer qualification problems. A 20-year-old roof in Miami-Dade is not just a deferred maintenance item. Many insurers will not write competitive policies on aging roofs, which means financed buyers cannot qualify or face insurance rates that destroy their debt-to-income ratios. Roof replacement runs $15,000 to $25,000 for most single-family homes and tends to recover its full cost at sale by reopening the buyer pool to financed purchasers.

Kitchen and bathroom refreshes (not gut renovations) can justify HELOC financing when the project cost stays disciplined. A $12,000 to $18,000 kitchen refresh in a South Miami home with a $700,000 price ceiling is financeable. A $55,000 gut renovation in the same home is not. The detailed breakdown of home updates that deliver pre-listing value covers exactly where the line falls for each project category.

Projects that do not justify financing: pools, full room additions, luxury appliance packages in mid-range markets. The resale recovery gap on these is too wide to absorb both the project cost and the debt service.

Are Home Improvements Tax Deductible? The IRS Rules Miami Homeowners Get Wrong

When Miami homeowners search "are home improvements tax deductible" before starting a project, most find a short answer that misses the more valuable explanation. The short answer is that improvements are not immediately deductible for personal residences. The longer answer is why that still matters for your finances.

The IRS draws a hard line between repairs and capital improvements. A repair restores something to its prior condition: fixing a broken window pane, patching a roof leak, repainting one room. Repairs are not deductible for personal residences and do not affect your cost basis. A capital improvement upgrades the home beyond its prior condition: replacing the entire roof, adding impact windows throughout, installing a new HVAC system, adding a bedroom or bathroom. Capital improvements are also not immediately deductible. But they increase your cost basis.

Your cost basis is what you paid for the home plus all documented capital improvements. When you sell, your taxable gain is the sale price minus your adjusted basis. Every dollar of qualified capital improvement you document in writing reduces that gain. For a Miami homeowner who has seen their property appreciate by $200,000 or more since purchase, this is not a minor accounting detail. It is a meaningful reduction in potential tax liability.

The IRS allows a capital gains exclusion of $250,000 for single filers and $500,000 for married couples filing jointly on the sale of a primary residence, provided the ownership and use tests are satisfied. For many Miami-Dade homeowners who purchased before 2022, that exclusion may not fully absorb their gain. Documented capital improvements are the legal mechanism for reducing the taxable portion of what remains. IRS Publication 523 covers the full rules for home sale exclusions and basis adjustments and is available directly from the IRS website.

Separately, certain energy-efficient home improvements qualify for the Energy Efficient Home Improvement Credit under IRS Form 5695. The credit equals 30 percent of qualifying project costs, up to an annual cap of $1,200 for most categories. Qualifying projects include exterior windows and skylights meeting Energy Star requirements, exterior doors, insulation, and certain HVAC systems. Miami homeowners installing impact windows that meet the Energy Star specification can claim this credit directly against their tax bill, not just as a reduction in taxable income. On a $20,000 window installation, a $1,200 credit reduces what you actually owe dollar for dollar. Details and updated eligibility requirements are on the IRS Energy Efficient Home Improvement Credit page.

One narrow exception: homeowners who dedicate a defined portion of their home exclusively to business use may be able to deduct a pro-rated share of certain improvements allocated to that space through the home office deduction. This is a specific exception with IRS requirements and does not apply to general renovations.

Tracking whether are home improvements tax deductible on a project-by-project basis, and keeping receipts and permits at the time of completion, is what separates Miami homeowners who exit a sale with a lower tax bill from those who pay more than necessary because they could not reconstruct their improvement history years later.

This section is for general informational purposes only and does not constitute tax, legal, or financial advice. Consult a licensed CPA or tax professional for guidance specific to your situation, filing status, and the nature of your improvements.

How to Sequence Your Top Home Improvements When You Are Using a HELOC and Watching the Tax Clock

Most homeowners choose projects based on what bothers them most. A smarter sequence prioritizes financial outcomes first.

Start with anything that currently creates an insurance or buyer qualification problem. A roof that is disqualifying financed buyers, an electrical panel flagged by inspectors, water intrusion that triggers disclosure obligations. These are not improvements. They are liabilities that erode your negotiating position every month they go unaddressed. Fix them first regardless of where they rank on any ROI list.

Second, fund the improvements that qualify for the energy efficiency tax credit. These are among the top home improvements with the clearest financial case when you are managing a HELOC draw alongside a tax calendar. If you are installing impact windows, replacing an HVAC system, or adding insulation, completing those projects in a tax year where you can capture the 30 percent credit reduces the effective cost of each upgrade. Spread multiple qualifying projects across consecutive tax years to capture the annual cap more than once.

Third, fund the cosmetic refreshes that move perceived condition from dated to updated. Kitchen cabinet fronts, vanity updates, flooring, landscaping. These belong later in the sequence because they carry shorter shelf lives before needing to be redone, and they produce no tax credits or insurance savings. Fund them from savings where possible. When the HELOC is the source, keep the draw small and the project scope disciplined.

Every piece of this sequencing starts from the same place: knowing your current equity position and where your home sits relative to comparable sales in your area. A current valuation tells you how much equity is available, which improvements will move the needle at resale in your specific zip code, and which ones will not. Getting a free home valuation is the step that makes every subsequent decision less speculative and more precise.

If you are thinking about the long game for your property, the upgrade decisions you make now and how you finance and document them directly shape your net proceeds at closing. Labrada Realty's seller resources are built around exactly that kind of long-game thinking.

For Miami-Dade homeowners with real equity and real renovation goals, the top home improvements worth pursuing are those that survive a three-part test: they produce a resale return that clears the financing cost, they qualify for a tax credit or meaningfully reduce your eventual capital gains exposure, and they address a condition problem that is currently limiting your buyer pool or your insurance options. Homeowners who apply that filter before spending tend to come out significantly ahead. Those who renovate based on personal preference alone often spend six figures improving their quality of life without improving their net equity position.

FAQ

Q: What is the difference between a capital improvement and a repair for tax purposes in Florida?

A: The IRS defines a capital improvement as work that adds value to your home, extends its useful life, or adapts it to a new use. Replacing a roof, installing impact windows, adding a new HVAC system, or building an addition all qualify. A repair restores something to its previous condition without adding value: fixing a leaky pipe, replacing a broken tile, or patching drywall. For Florida homeowners, this distinction carries real financial weight. Capital improvements increase your cost basis and reduce your taxable gain at sale, while repairs do not. Document every capital improvement with contractor invoices, material receipts, and permit records at the time of completion. Reconstructing that documentation years later is difficult and often incomplete.

Q: How much equity do I need to qualify for a home equity line of credit for home improvements in Miami-Dade?

A: Most lenders require a minimum of 15 to 20 percent equity to approve a HELOC, and they typically cap total borrowing at 80 to 85 percent of the current appraised value. On a Miami-Dade home worth $550,000 with a $300,000 mortgage, an 80 percent LTV ceiling gives you a maximum HELOC of $140,000, though your actual approved line will depend on your credit score, income, and debt-to-income ratio. Homeowners who purchased before 2021 generally have equity positions well above the minimum threshold given how much values have appreciated across Miami-Dade. A current home valuation is the first step before approaching a lender, both to confirm your actual equity position and to understand where your home stands relative to current comparable sales.

Q: Which top home improvements qualify for a federal energy tax credit in 2025 and 2026?

A: Under the Energy Efficient Home Improvement Credit, homeowners can claim 30 percent of qualifying project costs, up to an annual cap of $1,200 for most categories. Qualifying improvements include exterior windows and skylights that meet Energy Star requirements, exterior doors, insulation and air sealing materials, and certain high-efficiency HVAC systems and heat pumps. In Miami-Dade, impact windows that meet the applicable Energy Star specification qualify, which makes them even more financially compelling given their resale premium and insurance discount. The credit resets each tax year, so Miami homeowners planning multiple improvements across two years can capture the maximum credit annually rather than once. Claim it using IRS Form 5695 when filing your federal return.

Q: Does a HELOC affect my ability to sell my Miami home later?

A: Yes, but in a manageable way. A HELOC is a lien on your property, and the outstanding balance must be paid off at closing when you sell, alongside your first mortgage. In practice, sale proceeds handle both. Where sellers run into problems is when they have drawn the HELOC close to its maximum and the home sells for less than expected, leaving insufficient proceeds to cover all liens. In Miami-Dade's current market, equity positions are substantial enough for most homeowners that this scenario is uncommon for those who borrowed conservatively. The practical discipline is to keep HELOC draws proportional to the equity improvement the project is expected to deliver, not to the maximum amount the lender will approve.

Q: How do I calculate whether the home improvement return on investment justifies taking on debt?

A: Start with three numbers: the total project cost, the total interest you will pay over the repayment period, and the realistic resale premium the improvement adds in your specific zip code based on recent comparable sales. Add the first two and compare the sum to the third. If the resale premium exceeds the total cost including interest, the project pencils out on financing. If the gap is close, factor in whether the improvement also generates insurance savings or qualifies for an energy tax credit, either of which can close a marginal case. A home improvement return on investment calculation that uses national averages instead of local comparables will produce an answer that does not apply to your actual home, your actual market, or your actual buyer pool. Miami-Dade is not a national average market and should not be evaluated as one.

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Consult a licensed CPA or tax professional before making tax-related decisions about your home improvements, and consult a licensed mortgage professional for guidance on financing options specific to your situation.

Check out this article next