Most people searching for top real estate agents Miami end up on a directory page ranked by ad spend, review count, or transaction volume pulled from a national database. None of those metrics tell you whether that agent has ever closed a deal in the zip code you care about, understands Miami's condo approval timelines, or knows what Florida's property insurance crisis does to a financing contingency. This market is specific enough that the wrong agent does not just slow you down. They cost you money, leverage, and sometimes the deal itself. Here is what actually separates the best Miami realtors from everyone else, and how to verify it before you sign anything.

What "Top" Actually Means in the Miami Market

When a national site ranks Miami real estate agents, it is usually measuring volume. How many transactions closed last year. How many five-star reviews collected. How many zip codes listed in the agent profile.

Volume matters, but it is an incomplete picture. An agent who closed 80 transactions last year spread across Miami Beach, Homestead, Doral, and Hialeah may have done every one of those deals at a surface level: pricing pulled from automated reports, negotiations handled by assistants, no real sense of what buyers are paying per square foot in any one submarket.

The metrics that actually predict performance are narrower:

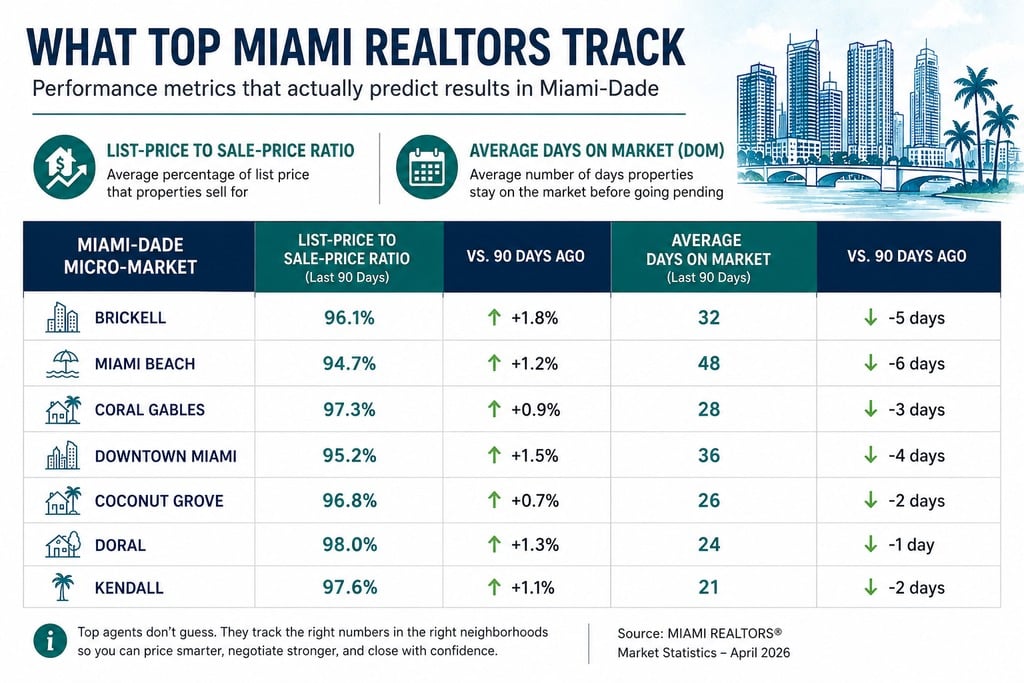

- List-price-to-sale-price ratio in the specific areas they work. Top Miami realtors who understand their market price correctly the first time. Agents who don't end up with 30-plus days on market and a price reduction before the first real offer.

- Local transaction depth. How many deals in this zip code, this building, this price tier. Not citywide volume.

- Days on market by area, not by agent. A good agent tracks DOM patterns by micro-market. If they can't tell you what the average days on market looked like in Kendall versus Coral Gables in the last 90 days, they are working from general knowledge, not live market intelligence.

The best Miami realtors are specialists operating at depth in a defined market, not generalists scattered across the county.

Why Miami Requires a Different Kind of Agent

Miami is not a proxy for U.S. real estate in general. The variables that drive deal outcomes here do not exist at the same intensity anywhere else in the country, and most agent-ranking systems do not account for any of them.

Foreign buyer concentration. A significant share of Miami transactions involves buyers from Latin America, Europe, and Canada. These buyers often pay cash, move on different timelines, and negotiate differently than domestic buyers. An agent who does not understand that dynamic misreads offers, misprices leverage, and sometimes walks away from a better deal because it did not look like the deals they are used to closing.

Condo association approval processes. In Brickell and Miami Beach especially, condo board approval can take 30 to 60 days after a contract is signed. Some buildings have rental restrictions, net worth requirements, or interview processes. An agent who does not know this going in will not protect you from a contract timeline that was never going to work. Top Miami realtors work with will already know which buildings run tight approval windows and which ones are predictable.

Seasonal demand patterns. Miami's market does not move evenly across the calendar. Demand from northern buyers and international visitors concentrates between November and April. Pricing power shifts. Sellers who list in January with a well-positioned agent capture a different buyer pool than sellers who list in August. The best agents plan around this. They do not just respond to the market, they anticipate it.

The insurance variable. Florida's property insurance market has tightened significantly over the past several years, and it now affects financing timelines in ways that were not a factor a decade ago. Lenders require wind mitigation reports. Insurability affects appraisal values. Some properties that look straightforward on paper hit friction at the financing stage because no one flagged the insurance exposure early. This is one of the most underestimated variables in Miami real estate right now.

The Questions That Separate the Best Miami Realtors From Everyone Else

Before you hire anyone, run this filter. It takes 15 minutes and it will tell you more than any directory ranking.

Ask them about the last three deals they closed in your target area. Not their overall volume. The specific streets, the price per square foot, the days on market, and what drove the outcome. A good agent talks about deals the way a practitioner talks about their work: with texture and detail. A generalist gives you a number and moves on.

Ask what the current average days on market is for your price point in your target zip code. If they have to check their phone to answer, that is useful information.

Ask whether they hold any licenses beyond a real estate license. This matters more in Miami than most markets. An agent who also holds a mortgage broker license can identify financing problems before they become contract failures. An agent with a title background understands what title issues look like and how to resolve them without blowing up a deal. Most buyers following a first-time buyer guide for Miami never think to ask this question, and they should.

Ask how they handle multiple-offer situations on the buy side. The answer reveals whether they know how to write a competitive offer in this market, or whether they default to the highest price and hope for the best.

Ask specifically about condo rules in any building you are considering. If they cannot speak to the association without looking it up first, they are not the right agent for that transaction.

How Neighborhood Expertise Changes the Outcome

Here is a concrete example of what local depth actually produces.

Two buyers, same budget, around $750,000. One is buying a single-family home in Kendall near SW 104th Street. The other is buying a condo in Brickell. Both hire agents with strong overall reviews but limited specific experience in those areas.

The Kendall buyer's agent prices their initial offer using county-wide comps. They miss that the Kendall micro-market at that price point has been running with multiple offers in under a week since early 2025. The offer comes in $15,000 below a number that would have been competitive. They lose the house and spend another 90 days searching.

The Brickell buyer's agent does not flag that the building they are targeting has a pending special assessment for facade repairs. The buyer finds out at the title stage. The deal collapses. They start over.

Neither of those outcomes happens with an agent who works that specific market every week. Local knowledge is not a soft advantage. It is a hard financial variable. You can see real examples of what that kind of market-specific work produces in the Labrada Realty success stories, or dig into the specifics of the Brickell market in the full Brickell buyer's guide.

What the Best Miami Realtors Know About the Insurance and Financing Trap

This section is the one most agent-guide posts skip, and it is where buyers lose deals they thought were already won.

Florida's property insurance market has been contracting for years. Several major carriers have exited the state. Premiums on waterfront and older properties have climbed sharply. And lenders are now scrutinizing insurability at the pre-approval stage, not just at underwriting. That sequence matters: a buyer can be pre-approved based on standard criteria, go under contract, and then discover that the property's insurance exposure pushes the monthly payment above what the lender will allow.

Top real estate agents Miami know this and run the insurance check early, before the offer goes in and not after the inspection period. For condos, they check the master policy status, the building's loss history, and whether the association's insurance is up to date. For single-family homes, they flag age of roof, proximity to flood zones, and whether a wind mitigation report has been done.

Sellers face a different version of the same problem. Listings with unresolved insurance issues attract lower offers and longer days on market because informed buyers price the risk. The best realtors in Miami advise sellers to resolve known insurance issues before listing, not after the first buyer walks.

This is also where having a mortgage broker in the same corner as your real estate agent changes the math. When your agent can see the full financing picture and not just the purchase side, problems get caught before they become contract failures.

How to Choose the Right Agent for Your Specific Situation

The framework is simpler than most people expect. It comes down to three variables: transaction type, area depth, and license breadth.

Transaction type. Buyers and sellers need different things from an agent. Buyers need someone who knows how to write competitive offers, reads market timing well, and protects them through the inspection and financing stages. Sellers need someone who prices correctly the first time, stages the listing for maximum first-weekend exposure, and knows how to manage multiple offers without leaving money on the table. Some agents do both well. Most have a natural strength in one direction.

Area depth. Use the explore Miami-Dade areas section of the Labrada Realty site to understand what the different micro-markets look like. Then ask your agent to show you their closed transactions in that specific area over the last 12 months. Not their team's transactions. Theirs. This is the filter that separates truly local miami real estate agents from professionals who list every zip code on their profile but work none of them deeply.

License breadth. In a market as complex as Miami, the agents who deliver the best outcomes are not just real estate licensees. They understand mortgage structure, title exposure, and the full closing timeline. Alberto Labrada holds a Florida real estate broker license, a mortgage broker license, and a title agent license. That triple-license model means buyers working with Labrada Realty get one point of contact who can see the entire transaction: financing structure, title risk, and pricing strategy. Three separate professionals who may not be communicating with each other is the alternative.

That matters most when something unexpected happens. And in Miami, something unexpected almost always happens.

For buyers who are early in the process, the buyers page at Labrada Realty walks through what working with the right agent actually looks like from search through close.

What to Do Before You Hire Anyone

Run three checks before committing to any agent.

First, verify their Florida real estate license at myfloridalicense.com. It takes 60 seconds and confirms they are active, in good standing, and what license type they hold. You can also check for any disciplinary history.

Second, ask for a list of closed transactions in your target area. Not testimonials, not a volume badge. Actual addresses and closing dates. Any serious agent will have this available.

Third, read the Florida Realtors guidance on what buyers and sellers can expect from a licensed agent in terms of fiduciary duty and representation standards at floridarealtors.org. Most people skip this step and do not understand what their agent is actually obligated to do on their behalf until something goes wrong.

If you want a starting point that skips the research entirely, the Consumer Financial Protection Bureau publishes guidance on working with real estate and mortgage professionals at consumerfinance.gov, useful context if you are navigating this for the first time.

The market rewards preparation. The buyers and sellers who close at the best terms are almost always the ones who did the work on the front end, including choosing the right agent before the search ever started.

FAQ

Q: How do I know if a Miami real estate agent is actually licensed?

A: You can verify any Florida real estate license in under a minute at the Florida Department of Business and Professional Regulation website, myfloridalicense.com. Search by name or license number. The result will show whether the license is active, the license type (sales associate versus broker), and any disciplinary actions on file. In Miami, where a significant share of the market involves unlicensed referral networks and international buyers who may not know what to ask, this check matters more than it does in most other states. Never sign a buyer or listing agreement without confirming the agent's license status first.

Q: What is the difference between a realtor and a real estate agent in Florida?

A: Every realtor is a licensed real estate agent, but not every real estate agent is a realtor. The term "realtor" specifically refers to a member of the National Association of Realtors, which requires adherence to a code of ethics beyond the state licensing standard. In Florida, licensed real estate agents must complete 63 hours of pre-licensing education and pass a state exam. Brokers must meet additional requirements including experience hours and a separate broker exam. When hiring in Miami, the broker designation matters because brokers carry more legal responsibility for transactions and typically have deeper market experience.

Q: How many homes should a top Miami realtor close per year?

A: There is no universal number, and volume alone is a misleading benchmark in Miami. An agent closing 15 to 20 transactions per year in Coral Gables or Key Biscayne, where median prices run well above $1 million, is operating at a different level of market depth than an agent closing 50 transactions per year spread across the county at entry-level price points. What matters more than raw volume is concentration. Look for agents who close multiple transactions in your specific area, at your specific price tier, year over year. That pattern shows genuine local expertise, not just activity.

Q: Do I need a different agent for a condo versus a single-family home in Miami?

A: Not necessarily a different agent, but absolutely a different set of skills from the same agent. Condo transactions in Miami involve layers that single-family deals do not: condo association approval timelines (which can run 30 to 60 days in Brickell and Miami Beach), building-level special assessments, master insurance policy status, rental restriction rules, and lender eligibility for the specific building. Some buildings are not warrantable, meaning conventional financing is not available. An agent who primarily works single-family homes may not know to check any of these before the contract is signed. If you are buying a condo, ask your agent to walk you through the building's approval process and insurance situation before you make an offer.

Q: Can the same agent represent me for the purchase and the mortgage in Florida?

A: In Florida, a licensed mortgage broker and a licensed real estate agent can be the same person, provided both licenses are active and the dual role is disclosed. This is not common, but it is legal and in some cases genuinely advantageous. When your agent also holds a mortgage broker license, they can see the financing picture at the same time as the purchase strategy, which means problems get caught earlier. Alberto Labrada holds a Florida real estate broker license, a mortgage broker license, and a title agent license, which means buyers working with Labrada Realty have one professional overseeing all three components of the transaction rather than coordinating between three separate parties.

Check out this article next