Most people assume first home buyer mistakes happen at the offer stage. They don't. They happen weeks earlier, in decisions that felt completely reasonable at the time: choosing a lender based on a rate quote, skipping an insurance check until the final week, making a competitive offer without understanding how Miami-Dade sellers actually evaluate one.

By the time those choices become visible problems, you're already deep in a transaction you can't easily unwind.

South Florida has its own rules. Condo boards that can reject your application after you've gone under contract. Insurance carriers that can change what your lender will fund. Listing agents who read your pre-approval letter in 30 seconds and know whether your offer is real. The buyers who close well here are the ones who understood those rules before they started shopping. The ones who didn't tend to find out at the worst possible moment.

Here is what actually goes wrong, and what to do instead.

The Pre-Approval Mistake That Kills Offers Before They're Read

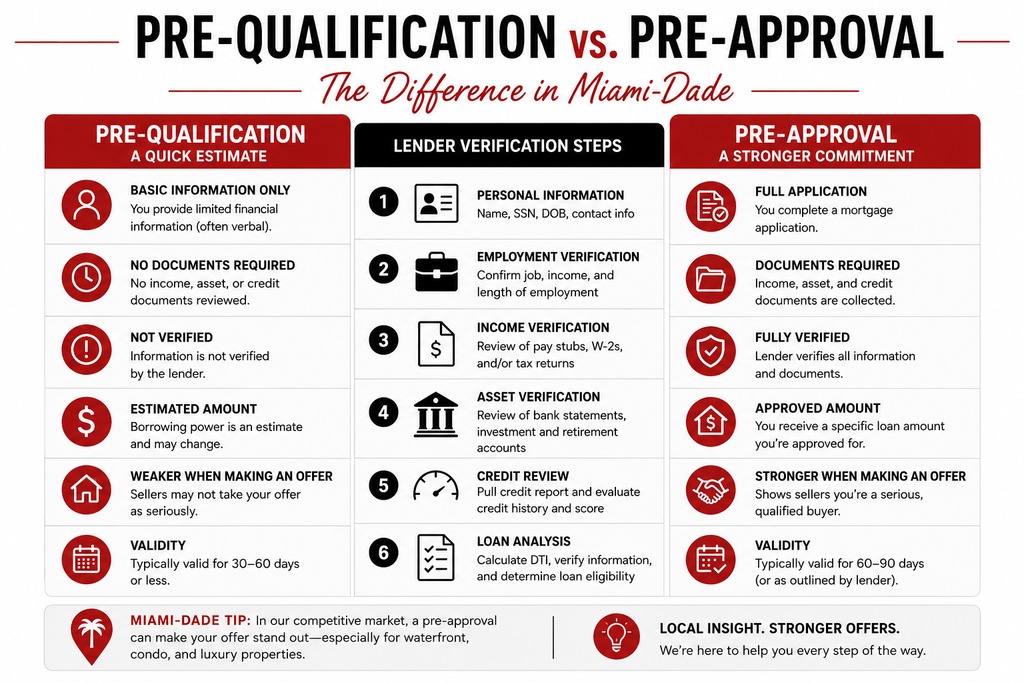

Among the most consistent first-time home buyer mistakes is treating a pre-qualification letter like it carries the same weight as a full pre-approval. It doesn't, and listing agents in Miami know the difference immediately.

Pre-qualification is an estimate. A lender took your word for your income and debt load and ran a quick calculation. Nothing was verified. A pre-approval means the lender pulled your credit, reviewed your pay stubs, tax returns, and bank statements, and confirmed you can borrow a specific amount under specific conditions. One tells a seller you might be able to buy their home. The other tells them you can.

In a market where well-priced homes in Kendall, Doral, and Palmetto Bay regularly receive multiple offers within the first weekend, a pre-qual letter signals uncertainty. Sellers move to the next offer.

The strongest position you can arrive in is a fully underwritten pre-approval, sometimes called a credit-approved pre-approval, where your file has already cleared underwriting before you find a property. On a $550,000 home in West Kendall, that one step can win a deal over a higher offer that came in with weaker financing.

One important note: what you do after getting pre-approved matters as much as getting it. The financial behaviors that can undo a pre-approval between offer and closing are covered in a later section.

Pricing Assumptions That Cost Miami Buyers Their Offers

One of the more expensive first home buyer mistakes in this market is walking in with a negotiation mindset built for a different city.

The logic sounds reasonable: list price is a starting point, leave yourself room to negotiate, offer lower and work up. In some markets, that works. In Miami-Dade, for correctly priced homes in active price ranges, it signals that the buyer doesn't understand the market. Sellers respond accordingly.

A specific example from 2024: a 3-bedroom, 2-bath home listed at $495,000 in The Hammocks area of Kendall received four offers in its first weekend on the market. A buyer opened at $449,000, citing room to negotiate. The seller did not counter. They moved to the next offer. The home sold at $505,000 to a buyer who came in at full asking price with a stronger financing package.

Miami-Dade single-family homes in the $400,000 to $700,000 range have averaged fewer than 30 days on market through recent cycles. Inventory in desirable areas near good schools or major employment corridors moves faster. A lowball offer in that environment isn't a negotiation. It's a rejection waiting to happen.

Understanding how to read a market before making an offer changes everything about how you compete. What investors know that most buyers don't is a useful framework for thinking about this differently.

The Inspection and Condo Approval Reality No One Explains

Skipping the home inspection to look more competitive is near the top of the list of what not to do when buying a house in South Florida. A missed roof condition in Miami-Dade, where full replacements run $25,000 to $45,000 on a mid-size home, is not something you negotiate after closing. Neither is an aging HVAC system or undisclosed water intrusion. The inspection is not a formality. It is your only window to find out what you are actually buying.

For condo buyers, there is a second layer that catches most first-timers completely off guard: board approval.

Many condo associations in Miami-Dade require formal buyer approval before a sale can close. The process involves an application, financial statements, background checks, reference letters, and sometimes an in-person interview with the board. Timelines range from two weeks to 60 days depending on the association. Some boards also hold a right of first refusal, meaning the association itself can step in and purchase the unit under the exact terms you negotiated.

If your contract does not include protective language for this window, and your financing timeline does not account for the delay, you can find yourself past your rate lock, at risk of losing your deposit, or being forced to close under conditions that no longer make sense.

This is a Miami-specific dynamic that buyers relocating from other states almost never anticipate. For a full list of behaviors that put buyers at risk during the purchase process, things you should never do when buying a home covers the details.

What Buyers Get Wrong About South Florida Insurance Before Closing

Most buyers budget for the mortgage. Very few budget correctly for what insurance will actually cost in South Florida, and the number tends to surface at exactly the wrong moment in the transaction.

Florida's property insurance market is unlike any other state. Wind mitigation ratings, flood zone designation, roof age, construction type, and distance from the coast all drive pricing. A townhome in a non-flood zone in South Miami might carry annual premiums of $3,000 to $4,500. A single-family home near Miami Beach in a high-velocity wind zone can run $8,000 to $14,000 per year or higher, depending on roof condition and construction year.

Here is where it becomes a financing problem: lenders require proof of insurance before they fund the loan. If you are seven weeks into a transaction, through inspection and appraisal, and your insurance quote comes in at $7,200 per year when you budgeted $2,400, your debt-to-income ratio has changed. Your lender may require a full re-underwrite. Your rate lock may expire. Your closing can slip, or fall apart.

The correction is simple but almost never made early enough: request an insurance quote during the due diligence period, not at the end of it. Get two or three quotes before you remove your financing contingency. That number needs to be part of your budget before you are committed to the deal.

Also worth knowing: Citizens Insurance, Florida's state-backed insurer, has been reducing its exposure and tightening eligibility requirements. Buyers who assumed Citizens would be the backup option are finding it either unavailable or significantly more expensive than it was two years ago.

Mistakes That Can Derail Mortgage Application After Pre-Approval

Mistakes that can derail mortgage application approvals don't always happen before you go under contract. Many of the most damaging ones happen after, during the weeks between signed contract and closing day, when buyers relax and make financial moves that feel unrelated to the transaction.

They are not.

Between the date a lender issues your pre-approval and the date they fund your loan, your financial profile is still being reviewed. Lenders often pull credit again within 48 hours of closing. These are the specific behaviors that have killed closings in Miami-Dade:

- Opening a new credit account for furniture, appliances, or moving costs: new accounts change your credit score and add monthly obligations, which shifts your debt-to-income ratio.

- Changing jobs, even to a better position: lenders want to see employment stability. A job change mid-transaction, including a promotion or a lateral move, can require a full file re-evaluation. Salaried employees who move to commission-based pay face the steepest hurdle, since lenders typically require two years of commission history to count it.

- Large deposits without documentation: if $15,000 appears in your bank account two weeks before closing without a clear paper trail, underwriting will hold the file. Gifted funds require a signed gift letter. Transferred funds need a documented source.

- Large purchases, even with cash: a car, appliances, or anything significant changes the financial picture your lender approved. New inquiries show up. New balances show up. Neither is invisible.

The practical rule for the period between pre-approval and closing: do not open anything, close anything, change anything, or spend anything large without talking to your lender first. This is one of the most common mistakes that can derail mortgage application progress, and one of the most preventable.

What to Do Instead at Every Stage of the Process

Avoiding first home buyer mistakes comes down to one thing: building your process around how this market actually works, not how you assumed it would work.

Before you search, get fully underwritten, not just pre-qualified. Know the difference between your maximum borrowing limit and what you should actually spend. In Miami-Dade, carrying costs including insurance, HOA fees, and property taxes can add $1,200 to $2,000 per month on top of your principal and interest on a $550,000 home, depending on property type and location.

During the search, work with someone who knows the specific area you are targeting at a granular level. Pricing dynamics in Doral are not the same as in Coral Gables. The pace of offers in Brickell condos is not the same as in Homestead. What reads as overpriced in one zip code is a discount in another. You can browse available properties in Miami-Dade to get a live picture of what is on the market and how inventory is moving right now.

During due diligence, do not waive protections to win a deal you are not prepared to own as-is. There is a version of competitive that is smart. There is another version that puts your deposit at risk. The difference usually comes down to how the offer is structured, not just what it says on price.

After going under contract, protect your financing the same way you protected your credit score to earn the pre-approval. Nothing changes until the keys are in your hand.

If you want to start the process with a team that knows these patterns from the inside, our VIP home search gives you access to off-market and early inventory across Miami-Dade, plus guidance calibrated to where you actually are in the process.

Still weighing whether now is the right time to stop renting? Should I rent or buy right now walks through how to think about that decision with current market context.

FAQs

Q: What are the most common first-time home buyer mistakes that people make before going under contract?

A: Most first-time home buyer mistakes before contract happen in three areas: arriving with a pre-qualification instead of a full pre-approval, making offers without understanding how that specific micro-market is moving, and underestimating total carrying costs including insurance, HOA fees, and taxes. In Miami-Dade, those three errors alone can result in lost offers, budget shortfalls at closing, or both. Buyers who take the time to get fully underwritten and run realistic carrying cost estimates before they start shopping close with far less stress and far fewer surprises.

Q: How do condo association rules affect buyers specifically in Miami-Dade?

A: Condo board approval in Miami-Dade can add anywhere from two weeks to 60 days to a transaction timeline, depending on the association. The process typically requires financial statements, references, background checks, and sometimes a board interview. Some buildings also hold a right of first refusal, allowing the association to purchase the unit under the same terms you negotiated. Buyers who don't account for this window in their contract timelines can end up with expired rate locks or financing that no longer works. Contract language protecting the buyer's deposit during the board approval period is not optional. It's essential.

Q: Is it ever a good idea to skip the home inspection to be more competitive in Miami?

A: Skipping the inspection is one of the clearest examples of what not to do when buying a house in South Florida. Roof replacements in Miami-Dade typically run $25,000 to $45,000. Full HVAC replacements run $7,000 to $15,000. Water intrusion issues in older construction can exceed both. A better approach is to compress the inspection timeline rather than remove it. Scheduling your inspector immediately upon contract execution and using findings as a negotiating tool keeps you competitive without leaving you exposed to costs you cannot see yet.

Q: How much should first-time buyers budget beyond the down payment in South Florida?

A: Beyond the down payment, buyers should plan for closing costs of 2 to 4 percent of the purchase price, property insurance ranging from $3,000 to $14,000 annually depending on the property's location and construction, documentary stamp taxes, title insurance, and prepaid escrow amounts. HOA fees, where applicable, can add $200 to $1,500 per month. On a $500,000 purchase, total out-of-pocket costs at closing, separate from the down payment, often run between $12,000 and $22,000. Buyers who only plan for the down payment tend to hit a cash shortfall in the final two weeks of the transaction.

Q: What specific financial behaviors are most likely to become mistakes that can derail mortgage application approvals in Miami?

A: The behaviors that most reliably surface as mistakes that can derail mortgage application approvals after pre-approval are opening new credit accounts, changing employment (especially from salary to commission), making large deposits without documentation, and financing any significant purchase before closing. Miami-Dade lenders frequently pull credit again within 48 hours of the closing date. New accounts, new balances, and new inquiries all show up. The safest rule from pre-approval to closing is to change nothing in your financial life without first clearing it with your lender.

If you want to know exactly where you stand before you start making offers in Miami-Dade, a 15-minute conversation can eliminate most of the surprises. Get a free home valuation if you already own a property, or reach out directly to talk through your buying timeline, realistic budget, and what the market looks like right now in the areas you are considering.

Check out this article next