Most buyers searching for multi family homes for sale in Miami picture one thing: a duplex where the tenant pays the mortgage. It is a smart idea, and in Miami, it can absolutely work. But the search gets complicated fast. Townhouses show up alongside duplexes in listings. "Multifamily" means something different to a lender than it does to a zoning office. And the neighborhoods where these properties actually trade at reasonable prices are not always the ones buyers expect.

Getting this wrong is not just confusing, it costs money. Buyers who make offers on properties they cannot finance, or who close on a townhouse expecting rental flexibility that the HOA prohibits, learn these lessons at the worst possible time. This guide walks through how each property type works in Miami-Dade, what financing actually looks like, where the inventory lives, and what moves buyers need to make before someone else does.

The Three Property Types Miami Buyers Often Confuse

Duplexes, townhouses, and small multifamily buildings all appear in the same search results. They are not the same thing.

A duplex is a single structure with two separate living units, each with its own entrance, kitchen, and utilities. Both units sit on one parcel under one deed. If you buy a duplex and live in one unit, you are an owner-occupant landlord. Lenders treat it that way, and it opens up financing options that purely investment-driven purchases do not get.

A townhouse is a single-family attached home. You own the interior and, in most cases, the land beneath your unit. There is no second unit to rent unless the floor plan was specifically built as a rental suite, which is rare and usually HOA-regulated. Many buyers searching for a duplex for sale in Miami end up looking at townhouses by mistake.

A small multifamily property is a building with three or four units on one parcel. These are classified as residential by lenders, not commercial, as long as there are no more than four units. That classification matters enormously for financing. A five-unit building follows a completely different loan process.

Knowing which type you want before you search is not a small detail. It shapes your financing, your zoning research, and the offer you submit.

How Financing Works Differently Across These Property Types

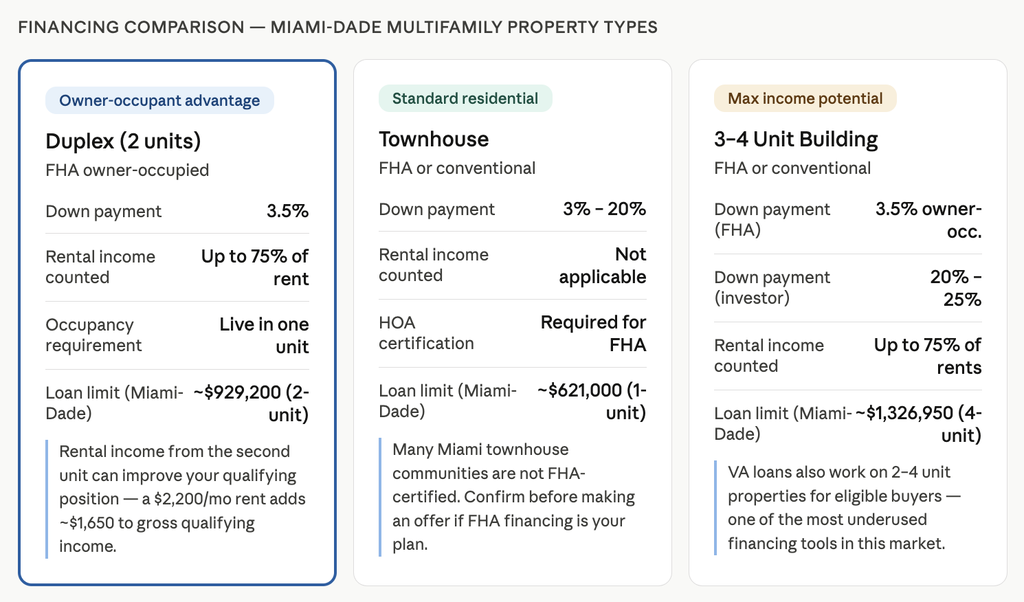

The most buyer-friendly financing scenario in Miami multifamily is the owner-occupied duplex purchased with an FHA loan. FHA allows as little as 3.5% down on a two-unit property, provided the buyer lives in one of the units. The reason this matters is that lenders will allow up to 75% of the projected rental income from the other unit to count toward your qualifying income. On a duplex renting for $2,200 per month, that is $1,650 added to your gross qualifying income, which can make a meaningful difference in how much mortgage you are approved for.

Townhouses qualify under standard FHA or conventional guidelines, same as a single-family home. The down payment range is 3% to 20% depending on the loan type and your credit profile. If you are buying a townhouse in a community with an HOA, the association itself has to meet FHA certification requirements for an FHA loan to work, and many Miami townhouse communities are not certified. Confirm this before you fall in love with a listing.

Three- and four-unit properties follow FHA multifamily guidelines. Down payments are typically 3.5% with FHA for owner-occupants, or 20% to 25% if you are buying as a pure investor with conventional financing. VA loans also work on two-to-four-unit properties for eligible buyers, which is one of the most underused financing tools in this market.

You can run the numbers on your mortgage before you talk to a lender. It gives you a baseline to work from in your conversations.

Where to Search for Each Property Type in Miami-Dade

Miami-Dade is not a monolith. The inventory for each property type concentrates in very specific areas, and knowing where to look saves weeks of filtering through listings that do not fit your goal.

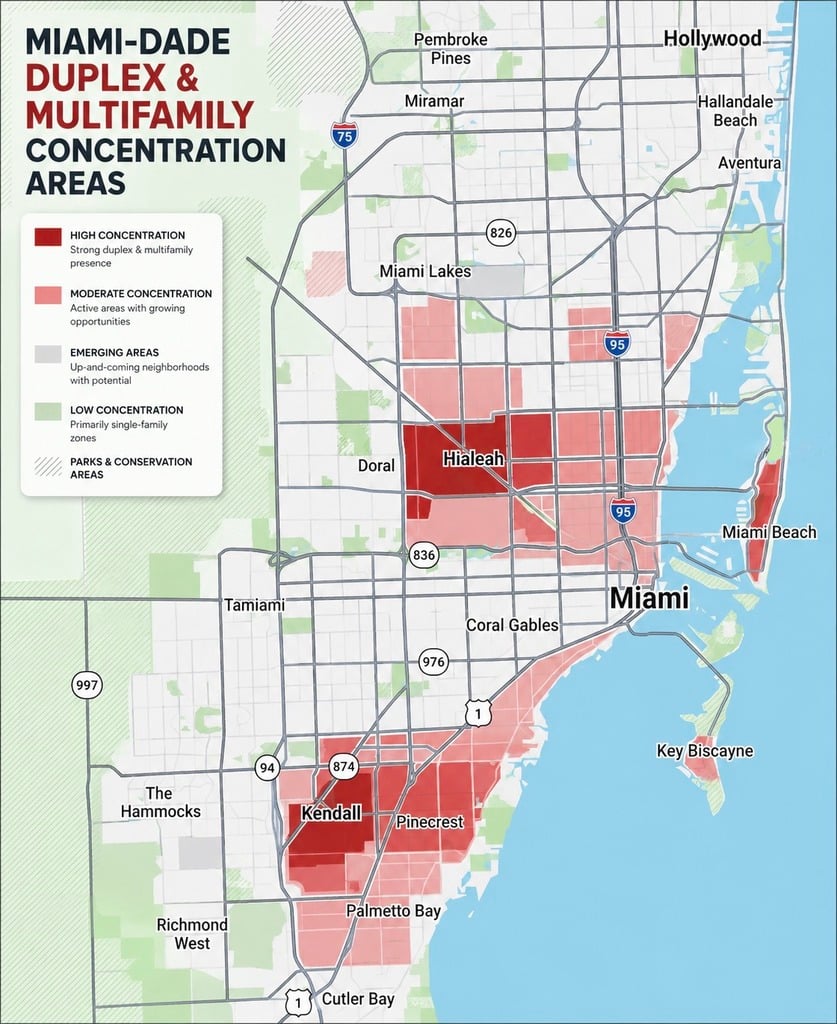

Duplexes are most common in older, established parts of the county. Little Havana, Westchester, Hialeah, and parts of West Miami have the highest concentrations of two-unit structures. These neighborhoods were built out in the 1950s and 1960s, when duplex construction was the default for working-class homeownership. Many of those original structures are still standing, now trading at prices that reflect both their income potential and their renovation needs.

If you are searching for a townhouse for sale in Miami, the inventory shifts to newer master-planned communities. Homes in Doral have some of the heaviest townhouse concentrations in Miami-Dade, particularly in gated developments with amenities. Kendall real estate also carries strong townhouse supply, including both fee-simple and HOA-governed options. Pembroke Pines, Miramar, and parts of Hialeah Gardens are worth adding to that list.

Three- and four-unit buildings show up in Allapattah, Overtown, Little Haiti, and parts of Liberty City. These are areas where investor activity has picked up significantly since 2019, which has pushed prices and compressed returns. Buyers who were watching these zip codes two years ago and did not move have largely missed the pricing window they were waiting for.

The Labrada Realty explore areas pages give neighborhood-level detail for most of these markets.

The Pricing Reality for Duplexes and Townhouses in Miami

Generic numbers are not useful here because pricing varies sharply by location, condition, and unit configuration. But buyers need a working frame of reference.

In Westchester and Hialeah, duplexes in livable condition without major updates are trading in the $520,000 to $680,000 range as of early 2025. Properties that have been renovated in both units, or where both units are occupied with strong leases in place, are pushing higher. A well-maintained Westchester duplex that went on market in late 2024 with both units tenanted at market rent received four offers in the first week and closed above asking at $671,000. Investors and owner-occupants were competing on the same property, which is the dynamic buyers need to understand.

Investor demand in this market segment does not price like a primary home purchase. An investor calculates a cap rate and makes decisions quickly. An owner-occupant who is slower to move, or who needs extra time for financing, often loses. Pre-approval before you search is not optional.

Townhouses in Doral are generally priced between $500,000 and $800,000 depending on size, community, and HOA fees. Townhouses in Kendall with no HOA, or with low HOA fees, carry a premium because the carrying cost math works better for buyers. HOA fees in some Doral communities run $400 to $600 per month, that is $5,000 to $7,200 per year in cost that does not go toward your equity and has to be factored into your affordability.

What Buyers Miss on the Purchase — and Pay For Later

The most common mistake on a duplex purchase is underestimating insurance costs. A two-unit structure in Miami-Dade does not insure the same way a single-family home does. Landlord policies on duplex structures, combined with windstorm coverage through Citizens or a private carrier, can run $8,000 to $14,000 annually depending on the age of the roof, construction type, and square footage. Buyers who model their cash flow using single-family insurance estimates end up surprised when the first renewal lands.

On townhouses, the frequent miss is the condo association approval timeline. Even though a townhouse feels like a house, many Miami townhouse communities are legally structured as condominiums. That means a condo association has the right to approve or deny buyers. Some communities have a review process that takes 30 to 45 days. If your contract has a 30-day closing window and the association needs 45 days, you either renegotiate the timeline or you are in breach. Buyers who did not check this before making an offer have had to extend closings at cost, or lose deposits when sellers would not accommodate.

Zoning is the third area where buyers get into trouble, particularly on duplex purchases. Not every structure marketed as a duplex has legal confirmation of dual-unit use. A property that was converted from a single-family home without proper permits is still legally a single-family home in the eyes of the county. Renting both units creates legal exposure, and financing gets complicated if the appraiser finds the second unit does not meet code. Always request a zoning confirmation letter from Miami-Dade before removing due diligence contingencies.

The buyer resources at Labrada Realty walk through what to verify at each stage of a purchase like this.

How to Move Fast When the Right Listing Appears

Buyers serious about multi family homes for sale in Miami need to be positioned before they start searching, not after they find something.

That means a fully underwritten pre-approval, not a pre-qualification letter, from a lender who has done FHA duplex or multifamily transactions in Miami-Dade specifically. Lenders unfamiliar with how rental income is counted under FHA guidelines, or with Miami-specific insurance requirements, slow closings down and sometimes kill them entirely.

It also means having your search parameters set precisely. Are you buying for owner-occupancy or as a pure investor? That determines your loan product, your down payment, and how you structure your offer. Sellers of income-producing properties care about your financing contingency, your timeline, and whether you understand what you are buying. An offer that signals buyer competence, a clean pre-approval, a realistic timeline, and no unnecessary contingencies, moves to the front of the consideration set.

If you are still in the early stages of deciding whether to buy or rent before this purchase, the rent vs. buy breakdown is worth reading. It puts the financial logic in plain terms.

For buyers who are ready to search: the active listings for a duplex for sale in Miami, a townhouse for sale in Miami, and multi family homes for sale in Miami are updated continuously on the site.

Miami-Specific Factors That Shape Every Multifamily Purchase

Insurance market pressure on financing timelines

Miami-Dade's insurance market has tightened significantly since 2022. Several private carriers have exited the state, and buyers of duplex and multifamily properties are increasingly routed to Citizens Property Insurance or a small number of remaining private carriers. The issue this creates is not just cost, it is timeline. Insurance binding, which lenders require before closing, is taking longer. On older structures, insurers may require a wind mitigation inspection, a four-point inspection, or both before issuing a quote. Buyers who wait until the last week of a 30-day closing to secure insurance are gambling. Start the insurance process the day your offer is accepted.

Seasonal demand patterns by price point

Miami multifamily demand is not uniform across the year. The October through April window draws more buyer activity overall, which means inventory moves faster and multiple-offer situations are more common on well-priced properties. Summer listings, May through August, sometimes sit longer, which creates real negotiating room for buyers who are willing to transact in the off-peak window. A duplex for sale in Miami that sat for 45 days in July may be the same property that would have gone under contract in a weekend the prior December.

HOA-heavy communities vs. non-HOA dynamics

For townhouse buyers, the HOA question is not just about fees. HOA-governed communities in Miami often have rental restrictions that directly affect how you can use the property. Some communities cap the number of units that can be rented at any given time. Others have minimum lease term requirements, typically six or twelve months, that prohibit short-term rentals entirely. Buyers who plan to rent out a townhouse need to read the HOA documents, specifically the rules and restrictions, before they close. Declarations that run 80 to 120 pages are standard. That review is not optional if rental income is part of your plan.

FAQ

Q: Can I use an FHA loan to buy a duplex in Miami if I plan to rent out one side?

A: Yes, and this is one of the strongest financing tools available for owner-occupant buyers in this market. FHA allows a 3.5% down payment on a two-unit property as long as you occupy one of the units as your primary residence. The additional benefit is that lenders can use up to 75% of the rental income from the other unit to help you qualify. In Miami-Dade, where duplex rents on the occupied side often range from $1,800 to $2,500 per month depending on location, that income credit meaningfully improves your qualifying position. One condition to check: the property needs to meet FHA minimum property standards. Older duplexes in Hialeah or Westchester sometimes require repairs before an FHA appraisal clears.

Q: What is the difference between a townhouse and a duplex in Miami-Dade?

A: A duplex is two separate residential units within one building on one parcel, each with independent living spaces, entrances, and typically separate utility meters. A townhouse is a single attached home, one unit, one family, connected to neighboring units but not configured for two-household occupancy. The distinction matters for what you can do with the property after you close. A duplex allows you to live in one unit and rent the other. A townhouse does not, unless there is a built-in accessory unit and the HOA specifically permits rentals, which many in Miami do not.

Q: How much do duplexes sell for in Miami right now?

A: Pricing depends heavily on location and condition. In Westchester and parts of Hialeah, duplexes in decent condition are trading in the $520,000 to $680,000 range. Properties with both units updated, strong leases in place, and newer roofs are pushing above that. In Little Havana, older structures with deferred maintenance can still be found below $500,000, but they carry renovation cost that needs to factor into your offer. The range is wide enough that buyers need to analyze specific zip code data and current days on market before setting offer expectations.

Q: What should I look for in a multifamily property in Miami before making an offer?

A: Four things deserve priority attention before you commit. First, confirm the legal use: get a zoning verification from Miami-Dade to confirm the property is permitted for multi-unit occupancy. Second, check the roof age and condition, insurance carriers in Florida use this to determine insurability, and a roof older than 20 years can make a property uninsurable or very expensive to insure. Third, review the current lease terms if tenants are in place, including rent amounts, expiration dates, and any rent-to-own clauses. Fourth, run the actual income and expense numbers with real insurance quotes, not estimates. Many buyers skip step four and discover the cash flow math does not work the way they expected.

Q: Is a townhouse a good investment in Miami compared to a single-family home?

A: A townhouse for sale in Miami can be a strong investment under the right conditions, but it is not a straightforward comparison. Townhouses typically come with HOA fees that reduce net cash flow, sometimes significantly. However, they also carry lower maintenance responsibility for exterior elements and often sit in communities with strong demand from renters and buyers alike, which supports resale value. The comparison to a single-family home depends on price point, HOA terms, and rental restrictions in the specific community. A townhouse in a Doral community with a $500 monthly HOA and a 12-month minimum lease requirement has a very different investment profile than a no-HOA townhouse in a Kendall neighborhood with no rental cap.

If you are actively searching for multi family homes for sale in Miami and want to know which properties are actually available, what the realistic income looks like, and how to structure an offer that competes, let's connect. A 20-minute conversation is usually enough to clarify whether a specific property makes sense for your situation.

Check out this article next