Most buyers who come to me asking about foreclosures in Miami-Dade have the same picture in their head: a deeply discounted house, a motivated bank, and a straightforward path to a deal. Sometimes that picture is accurate. More often, it isn't. Foreclosed properties in this market carry a different set of rules, timelines, and risks than standard resale purchases, and the buyers who don't understand that going in are the ones who lose deposits, inherit debt, or close on a property they can't insure. These tips for buying a foreclosed home are built specifically around how Miami-Dade's foreclosure pipeline works, not how it works in a generic real estate guide written for no market in particular.

What "Buying a Foreclosure" Actually Means in Miami-Dade

Not all foreclosures are the same type of purchase, and confusing them is one of the first places buyers go wrong.

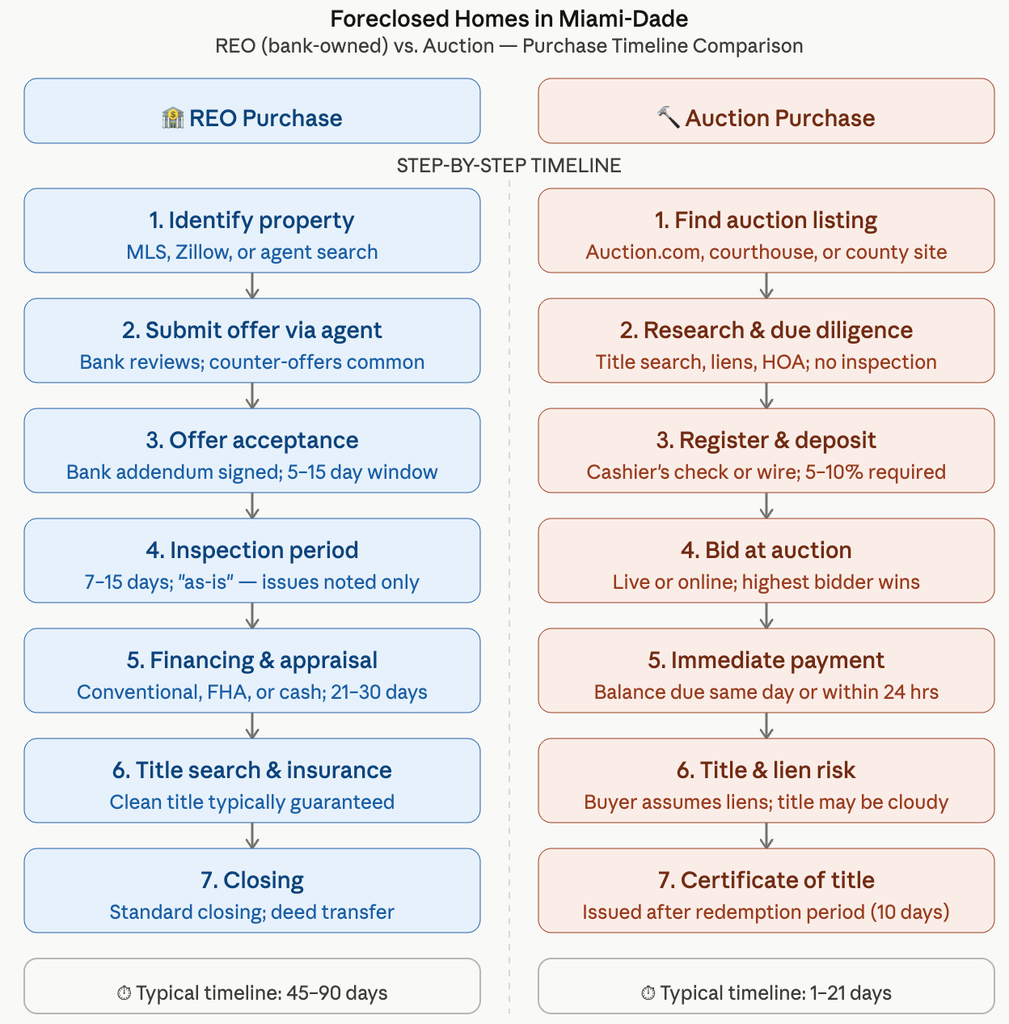

In Miami-Dade, buyers encounter two main categories. The first is bank-owned property, also called REO (Real Estate Owned). This is a home the lender has already taken back after the foreclosure process completed. It sits on the MLS, often listed by an asset management company on behalf of the bank. You make an offer, negotiate, and close through a relatively standard process, with one major exception: the seller is a bank, not a person, and they operate on their own timeline with their own addenda.

The second category is courthouse auction, which is where Miami-Dade holds its foreclosure sales online through the Clerk of Courts platform. These are competitive, fast-moving, and carry significantly more risk. You are often bidding on a property you have not been able to inspect, and if you win, you own it as-is, with no contingencies and no recourse.

Most first-time foreclosure buyers are better served starting with REO properties. Auctions reward buyers who have done this before, have capital reserves, and can absorb a surprise.

Understanding which type you are pursuing changes every decision that follows.

The Miami-Dade Foreclosure Process, Step by Step

The process for buying an REO in Miami-Dade moves differently than a standard resale, and buyers who treat it the same way often lose the property or the deal.

Step 1: Get your financing squared away before you look.

Banks selling REO properties in Miami-Dade do not wait for you to figure out your loan. Most bank addenda include strict timelines, sometimes as short as 21 days to close. If your lender needs 45 days, you are already in conflict before the ink dries. Get pre-approved, confirm your lender's timeline, and if you are considering a property that needs significant work, have a conversation with your lender about rehab loan options before you fall in love with a listing.

Step 2: Find the right listings.

Miami foreclosure listings appear across several channels: the MLS (the most reliable source for REOs), the Miami-Dade Clerk of Courts site for auction properties, and third-party platforms like Hubzu, Auction.com, and Xome for bank-managed sales. Each platform has different rules for offers, earnest money, and closing timelines. Knowing which platform a property is listed on tells you a lot about what the process will look like. You can browse current foreclosure homes for sale in Miami to see what is actively available across Miami-Dade right now.

Step 3: Submit a clean, competitive offer.

On REO properties, banks typically counter or respond within 3 to 10 business days. They are not emotionally attached to the property, but they are managing dozens of assets simultaneously. A clean offer, meaning one that is pre-approved, has a realistic closing timeline, and does not load up on unusual contingencies, moves faster through their review process. Sloppy offers with long inspection periods and weak earnest money get deprioritized.

A real example: A buyer I worked with was targeting a 3-bedroom REO in Kendall, listed at $389,000. The home had been sitting for 22 days, which in that price range told us the bank had already gotten low offers they rejected. We came in at $378,000, clean, with 10% earnest money and a 30-day close. The bank countered at $385,000. We settled at $381,500. The property appraised at $394,000. The buyer had $12,500 in built-in equity on day one, before any repairs. That outcome was not luck. It came from reading the listing correctly and structuring the offer around what the bank actually needed.

What Inspections and Due Diligence Look Like on a Foreclosed Home

This is where buyers get into serious trouble, and it is one of the most important tips for buying a foreclosed home in any market, but especially in Miami-Dade.

Foreclosed properties sell as-is. The bank is not going to fix the roof, remediate the mold, or address the unpermitted addition the previous owner built in the garage. What you see is what you get, and what you do not see is your problem the moment you close.

Standard due diligence on a foreclosed home in Miami-Dade should include:

- A full home inspection by a licensed inspector, with specific attention to roof condition, HVAC age, plumbing, and any signs of water intrusion. Miami's humidity is not forgiving to deferred maintenance.

- A wind mitigation inspection, because this directly affects your insurance quote, which directly affects whether your loan can close.

- A four-point inspection if the home is older than 20 years, again for insurance purposes.

- A title search, without exception. More on this in the next section.

- A drive-by or walkthrough to confirm occupancy status. Foreclosed homes in Miami-Dade sometimes have tenants, occupants, or squatters. Finding this out before closing is significantly better than finding it out after.

One thing many buyers skip: pulling the property's permit history through Miami-Dade's online permit portal. Unpermitted work does not disappear when the bank sells the property. It transfers to you, along with any open violations. A $15,000 unpermitted addition that needs to be demolished or properly permitted is not a discount. It is a liability.

The Financing Reality Most Buyers Do Not See Coming

Financing a foreclosed home in Miami-Dade is not always straightforward, and the mismatch between buyer expectations and lender requirements kills a meaningful number of deals.

Conventional loans work on foreclosures, but only when the property meets minimum condition standards. A home with a damaged roof, no functioning kitchen, or significant structural issues will not pass an appraisal for a conventional loan. FHA loans add another layer: the property must meet HUD's minimum property requirements, which are stricter than conventional guidelines.

If the property needs work to be financeable, buyers have a few realistic options:

- FHA 203(k) loan: Allows you to finance both the purchase and renovation costs in a single loan. It is slower to close and requires a HUD-approved consultant, but it is a legitimate path for properties that need moderate rehabilitation.

- Conventional rehab loan (Fannie Mae HomeStyle): Similar concept, slightly more flexible on property types, but requires strong credit and a lower debt-to-income ratio.

- Hard money or bridge loan: Fast, flexible, and expensive. This is how investors move quickly on foreclosed homes Miami Dade county listings when speed matters more than cost of capital. It is not the right tool for most owner-occupant buyers, but it is worth understanding.

Miami's insurance market adds a layer that does not exist in most other states. Getting a homeowner's insurance quote before closing is not optional on a foreclosure purchase here. Some properties, particularly older homes with aluminum wiring, aging roofs, or specific construction types, are difficult or impossible to insure at a cost that keeps the loan viable. Use the mortgage calculator to model different insurance scenarios before you commit.

Banks selling REO properties also set their own closing deadlines in their addenda, and those deadlines do not flex easily. If your lender needs more time than the bank allows, you may be looking at a per diem penalty or a cancelled contract. Line up your financing before you make an offer, not after.

Common Mistakes That Cost Buyers the Deal or the Property

Buying foreclosed homes Miami Dade county style, meaning fast, competitive, and as-is, punishes buyers who are not prepared. These are the mistakes that show up most often.

Skipping the title search.

This is the most expensive mistake a foreclosure buyer can make. Some foreclosed properties in Miami-Dade carry IRS liens, HOA super-liens, municipal code enforcement liens, or unpaid special assessments that survive the foreclosure and transfer to the new owner. A title search surfaces these before closing. Title insurance protects you if something is missed. Both are non-negotiable on a foreclosure purchase.

HOA debt deserves specific attention. Florida law gives HOA associations a super-lien for up to 12 months of unpaid assessments, and that lien attaches to the property, not the previous owner. If you buy a condo in a building where the prior owner owed $18,000 in back assessments and the HOA filed correctly, you may be walking into that obligation on day one. Your closing attorney or title company should identify this. If they do not, find different representation.

Misjudging repair costs.

Buyers who buy foreclosures in Miami-Dade without a realistic repair estimate often make one of two errors: they either overbid because they underestimate the work, or they walk away from a genuinely good deal because they overestimate it. Walk the property with a contractor, not just an inspector, before finalizing your offer. Inspectors identify what is wrong. Contractors tell you what it costs to fix it.

Moving too slowly.

Well-priced REO listings in Miami-Dade, particularly in areas like Kendall and Doral, do not sit. Multiple offer situations on foreclosures are common when the bank has priced the property correctly. Buyers who spend a week thinking about whether to submit an offer frequently find the property is already under contract. Pre-approved, prepared, and decisive is the posture that wins foreclosure deals in this market.

Also review things you should avoid when buying a home for a broader set of purchase missteps that apply to foreclosures with extra weight.

How to Find the Right Foreclosures and the Right Help in Miami-Dade

Miami foreclosure listings are not all in the same place, and knowing where to look depends on what type of purchase you are targeting.

For REO properties, the MLS is still the most reliable source. REOs listed through the MLS have been assigned to a listing agent, which means they come with a defined process, a point of contact, and a cleaner chain of documentation. These are the foreclosed homes for sale Miami buyers interact with most often, and they are the most accessible entry point for buyers using traditional financing.

For auction properties, Miami-Dade County runs its foreclosure auctions through the Clerk of Courts website. Sales are posted in advance, and the process requires same-day payment in full. These auctions attract experienced investors, cash buyers, and people who have done their homework on the specific property well before the auction date.

Third-party platforms like Hubzu and Auction.com carry a mix of bank-managed REOs and pre-foreclosure listings. The rules on these platforms vary. Some allow inspection periods; others do not. Read the asset manager's terms before submitting anything.

Working with an agent who understands this specific category of purchase matters more on foreclosures than on standard resale transactions. The paperwork is different, the timelines are different, and the negotiation dynamics are different. A general-practice agent who handles one foreclosure a year is not the same as someone who actively works this segment of the Miami-Dade market. If you want to search available properties in Miami-Dade and filter for what is currently active, that is a starting point. From there, having the right guidance on which listings are worth pursuing and how to structure an offer around a bank's specific requirements is what separates buyers who close from buyers who keep losing deals.

At Labrada Realty, we work with buyers across Miami-Dade on both REO purchases and auction strategies. The process is not complicated once you understand how it actually works, but it is specific. Getting the details wrong on a foreclosure purchase is more expensive than getting them wrong on a standard resale, because the seller will not negotiate repairs, extend timelines out of goodwill, or warn you about what they know. Preparation and local knowledge are what close these deals cleanly.

FAQ

Q: Can I buy a foreclosed home in Miami with a conventional loan?

A: Yes, but the property has to meet the lender's minimum condition requirements, and that is where many foreclosure deals fall apart. Conventional loans require the home to be in livable condition at the time of appraisal. A property with a damaged roof, missing appliances, or significant water damage will typically fail the appraisal. In that situation, buyers have to either bring cash, use a rehab loan, or find a different property. Miami-Dade has a wide range of foreclosed homes in different condition levels, so the financing path depends heavily on the specific property.

Q: Are there hidden costs when buying a foreclosure in Miami-Dade?

A: Several. Beyond purchase price and standard closing costs, foreclosure buyers in Miami-Dade should budget for: a full inspection, wind mitigation report, four-point inspection, title search, and title insurance. On top of that, outstanding HOA assessments, code enforcement liens, and unpermitted work can all transfer to the buyer at closing if not caught beforehand. Repair costs are the other major variable. A property that looks like a $30,000 discount can quickly become a breakeven or loss if the deferred maintenance is significant. Get a contractor walkthrough before you finalize any offer.

Q: How long does it take to close on a foreclosed home in Miami?

A: On a standard REO purchase with conventional financing, plan for 30 to 45 days from accepted offer to closing, assuming your lender is organized and the title comes back clean. Cash purchases can close faster, sometimes in 15 to 21 days, but the bank's asset manager still controls the timeline on their end. Auction purchases through the Miami-Dade Clerk of Courts require same-day or next-day payment in full, so "closing" happens almost immediately once you win the bid. The bigger risk on REO closings in Miami-Dade is not the calendar, it is the title. If a lien surfaces late or the title company needs additional documentation from the bank's loss mitigation department, delays of one to three weeks are common.

Q: What happens to liens and HOA debt when I buy a foreclosure?

A: Florida law allows certain liens to survive the foreclosure and transfer with the property, which surprises a lot of buyers. IRS tax liens, HOA super-liens for up to 12 months of unpaid assessments, and municipal code enforcement liens are the most common examples that show up on Miami foreclosure listings. A proper title search, conducted before closing, is the mechanism that identifies these. Your title insurance policy protects you if something is missed after closing, but it does not protect you from liens you were already aware of. Do not skip either step.

Q: Is buying a foreclosed home in Miami-Dade worth it right now?

A: It depends on what you are comparing it to. Foreclosures in Miami-Dade are not always deeply discounted relative to market value, especially in high-demand areas where inventory is tight. The advantage is not always in the price. Sometimes the advantage is in finding a property that has less competition than a move-in-ready listing, or accessing a price point you could not reach otherwise. For investors, the math is in the spread between purchase price plus rehab cost versus after-repair value. For owner-occupants, the math also has to include insurance, financing cost, and livability timeline. The deals exist. They just require more preparation than a standard purchase, and less emotional decision-making.

CTA

If you are ready to start looking at real foreclosure opportunities in Miami-Dade, not just browsing listings but actually understanding which properties are worth pursuing and why, browse current foreclosure homes for sale in Miami and reach out directly. We will walk you through what is active, what is actually priced well, and what the process looks like for your specific situation.

Check out this article next