Most people preparing to buy their first home spend weeks scrolling listings and comparing square footage. Almost nobody spends that same energy understanding what actually happens between making an offer and sitting at the closing table. In Miami-Dade, that gap is where deals fall apart, budgets get blindsided, and buyers end up in homes that cost them far more than they planned.

The real estate process here runs on a set of local rules that no generic first time home buyer tips and advice article will ever fully capture. Insurance costs have reshaped what you can actually afford. HOA approval timelines can derail even well-financed buyers. And the difference between a good-faith seller and one who has been overpriced for six months can mean thousands of dollars in negotiation leverage if you know how to read the situation.

This guide walks through each stage of the process the way it actually works in Miami, not the way the textbook describes it.

Start With the Numbers, Not the Listings

There is a reason lenders draw a hard line between pre-qualification and pre-approval, and it is not bureaucratic habit. Pre-qualification is a rough estimate based on what you tell a lender. Pre-approval is an underwritten determination of what you can actually borrow. In a market like Miami-Dade, where competitive listings can move in days, walking in with only a pre-qualification letter is the same as walking in with nothing.

Before you look at a single listing, get fully pre-approved. That means a lender has pulled your credit, verified your income documents, and reviewed your asset statements. It also means you know your real number, not a ballpark.

In Florida, lenders underwrite using a debt-to-income ratio (DTI) that typically cannot exceed 43% for most conventional loans. If you have a car payment, student loans, and minimum credit card payments already eating into that ceiling, your approved purchase price will be lower than the online calculators suggest. Run the actual numbers before you fall in love with a neighborhood.

One detail Miami-area buyers often miss: insurance costs must be factored into your monthly payment calculation. Homeowner's insurance in South Florida has increased sharply over the past several years. On a $500,000 home in Miami-Dade, annual insurance premiums can run anywhere from $5,000 to over $12,000 depending on the property type, age of the roof, and proximity to flood zones. Lenders include that cost in your monthly payment when calculating DTI, so the home you think you can afford may require a lower purchase price than expected.

Use the mortgage calculator at Labrada Realty to model a realistic monthly payment before you commit to a search range. Include taxes, insurance, and HOA fees as separate line items.

What Your Budget Actually Buys Across Miami-Dade

Miami-Dade is one county, but it functions like a dozen different markets stacked on top of each other. A budget of $450,000 means something very different in Homestead than it does in Kendall, and something entirely different again in Brickell or Coral Gables.

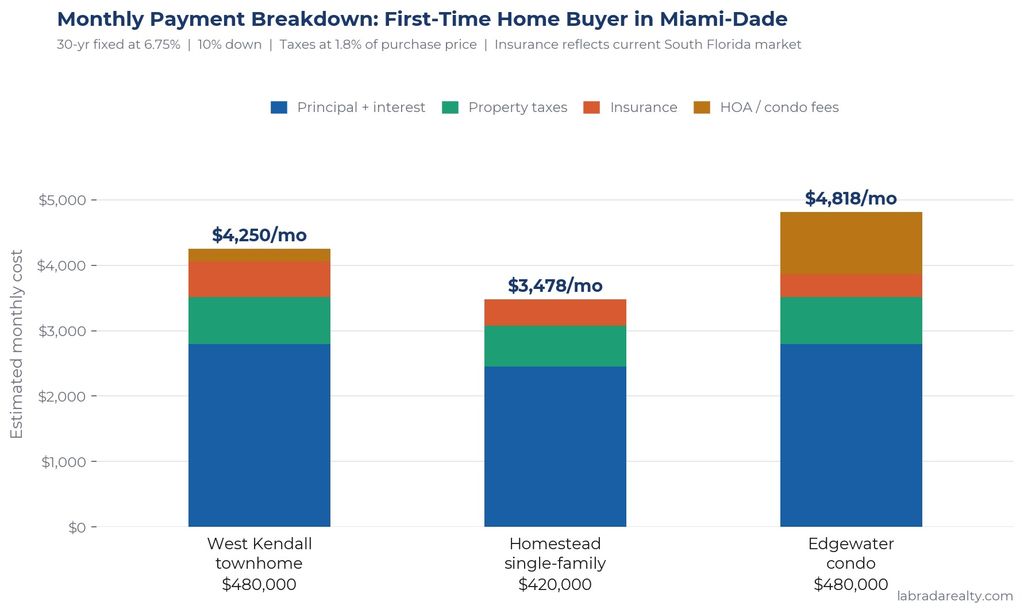

As of early 2026, the countywide median sale price sits around $575,000, with Zillow tracking typical values near $495,000. Entry-level inventory in established areas like Kendall and the Hammocks generally starts around $450,000 to $550,000 for a 3-bedroom, 2-bath single-family home. In Homestead, that same budget can reach a newer, larger home, sometimes in a community with fewer years of deferred maintenance. Down in Brickell, $450,000 will get you a one-bedroom condo, with monthly HOA fees often running $800 to $1,200 or more.

Here is the real-world example worth understanding: A buyer with a $480,000 budget who locks in on a townhome in West Kendall will likely be looking at a monthly payment around $3,100 to $3,400 all-in when taxes, insurance, and HOA are included. That same buyer focusing on a condo in Edgewater may find a unit at a similar purchase price, but with HOA fees that push the monthly total past $4,000. Both are in Miami-Dade. Both feel like $480,000. The effective cost is not the same.

Before you set your search range, spend time on the available listings in Miami-Dade and sort by total monthly cost, not just price. The purchase price is the starting line.

The Mistakes That Cost First-Time Buyers the Most

First-time home buyer tips rarely spend enough time on the errors that actually hurt people. Here are the four that show up most often in Miami-Dade transactions.

Making an offer without reading the seller's situation

A home that has been on the market for 90 days in Miami-Dade in 2025 and 2026 is a different negotiation than a home that hit the MLS three days ago. Countywide, average days on market have climbed to around 96 days. Sellers in that longer-DOM position are frequently more negotiable than their list price suggests. Buyers who walk in at asking price on a stale listing leave real money behind.

Waiving inspections under competitive pressure

Even in a multiple-offer situation, skipping the inspection on a Miami-area home carries significant risk. South Florida properties face specific issues that do not appear in other markets: roof age and condition, wind mitigation deficiencies, aluminum wiring in older homes, and foundation cracking in properties near coastal areas. An inspection waiver saves you a few hundred dollars and can cost you tens of thousands. There are ways to be competitive without eliminating your right to know what you are buying.

Forgetting to account for HOA fees in your budget

In HOA-heavy communities across Miami-Dade, which covers a substantial portion of the available inventory, monthly fees can range from $150 to over $1,000 depending on the community and what amenities are included. Those fees count against your DTI when a lender calculates your maximum loan amount. A buyer approved up to $500,000 with no HOA exposure may only qualify for $460,000 if the target property carries a $600 monthly HOA.

Opening new credit before closing

Financing your moving expenses with a new credit card, buying a car after going under contract, or co-signing a loan for a family member in the weeks before closing can kill a transaction. Lenders run a final credit check close to the closing date. Any new debt that changes your DTI can result in loan denial or a required reduction in the loan amount. Review the things you shouldn't do when buying a home before you go under contract.

How the Miami Market Actually Behaves

Understanding the mechanics of this market is where tips for buying your first home in Miami diverge most sharply from advice written for buyers anywhere else.

Insurance has changed what lenders will finance

Florida's property insurance market is in a period of significant stress. Several major carriers have exited the state, premiums have escalated, and many properties now require Citizens Property Insurance, the state-backed insurer of last resort. For buyers, this matters in two ways. First, some lenders are more conservative about financing properties in high-risk flood zones because the insurance costs compress the buyer's qualifying income. Second, the age of the roof on a target property can directly affect insurability. A roof older than 15 years may trigger surcharges or coverage denials that a buyer only discovers after going under contract.

Ask about roof age and existing insurance costs as part of your due diligence, before you make an offer.

Condo approval timelines can extend your closing

In Miami-Dade, buying a condo means buying into a two-layer approval process. The lender has to approve the building, and the association has to approve you as a buyer. For FHA or VA financing, only buildings on the approved list qualify. Many Miami condo buildings are not FHA-approved, which narrows your financing options significantly. Even with conventional financing, condo association review processes can add two to four weeks to a closing timeline. Budget for this when you write your contract.

Seasonal demand patterns by price point

Miami does not follow the classic spring-market pattern that dominates real estate advice written for northern cities. Activity in Miami-Dade can remain strong through late fall, particularly at the $600,000 and above price point, driven partly by buyers relocating from out of state who have more schedule flexibility. Entry-level buyers face less competition in summer months when inventory tends to sit slightly longer. If your budget is under $500,000, you often have more negotiating room from July through September than you will in January or February.

Down payment assistance programs are real and often overlooked

Miami-Dade County offers a Homebuyer Down Payment Assistance Program providing up to $35,000 in interest-free deferred loans for qualifying first-time buyers. Income limits are set at $95,620 for individuals and $136,500 for a four-person household. The Florida Hometown Heroes program provides up to $35,000 in down payment and closing cost assistance for eligible full-time workers. The Housing Finance Authority of Miami-Dade offers up to $15,000 in a deferred zero-percent second mortgage alongside a 30-year fixed first mortgage. These programs require homebuyer education, income verification, and working with an approved lender. Many buyers discover them too late in the process to use them. Get familiar with your options before you start the search.

Tips for Buying a New Construction Home in Miami

New construction has become an appealing option for many first-time buyers in Miami-Dade, particularly in areas like Homestead, West Kendall, and Doral where builder activity remains active. The appeal is understandable. No deferred maintenance, modern finishes, energy-efficient systems, and a warranty. But the tips for buying a new construction home that apply in Miami carry a few specific cautions.

The builder's sales rep works for the builder

This is the point most first-time buyers in new construction miss. The sales representative at the model home is an employee of the builder, or a contractor working exclusively for the builder. Their job is to get the best deal for the builder, which is not the same as getting the best deal for you. Bringing your own buyer's agent to a new construction purchase costs you nothing as a buyer (the builder pays agent commissions), and it gives you someone whose legal obligation runs to your interests, not the builder's bottom line.

Builder incentives often come with conditions

Builders in Miami's current market are offering incentives to move inventory: rate buydowns, closing cost credits, and upgrade packages. These can represent genuine savings. But many builder incentives are tied to using the builder's preferred lender. Before you accept an incentive package that requires using their financing, compare the full loan terms against what an independent lender would offer. A below-market interest rate for the first two years of a loan can cost you more than you save if the back-end rate resets higher, or if the builder's lender is adding margin elsewhere in the loan structure.

Inspect during construction, not just at the end

On a new construction home in Miami-Dade, you have the right to schedule independent inspections at key stages of the build: foundation, framing, rough-in plumbing and electrical, and final walkthrough. Many buyers skip interim inspections because the home is new and assume the city's permitting process catches everything. It does not. An independent inspector working for you will catch issues that are far cheaper to fix before drywall goes up than after.

New construction contracts in Florida are written by the builder's attorney and are heavily weighted in the builder's favor. Before signing, have the contract reviewed. Completion date language, what constitutes a material change in specifications, and how disputes are handled are all areas where first-time buyers can be caught off guard.

For a broader perspective on how to approach buying strategically, the guide on what buyers can learn from real estate investors covers some of the same due-diligence habits that apply whether you are buying resale or new construction.

From Research to a Real Decision: How One-Stop Guidance Changes the Process

Most first-time buyers piece together their buying team from separate sources: a real estate agent from one place, a lender from another, a title company their agent recommends. Each party has their own timeline, their own communication style, and their own priorities. When something goes sideways, which in Miami-Dade transactions it often does, the buyer ends up in the middle trying to manage three separate conversations.

The practical advantage of working with someone who handles real estate brokerage, mortgage financing, and title under one roof is that the process compresses. When the agent writing your offer is the same person managing your loan and the same team handling your title work, there is no translation loss between parties. Issues that would take days to resolve across separate vendors get handled in hours. For a first-time buyer navigating an unfamiliar process, that coordination reduces stress and materially reduces the risk of a transaction falling apart over a timing issue.

Alberto Labrada is a licensed Florida real estate broker and mortgage broker with title capabilities. First-time buyers working through Labrada Realty's buyer resources move through the process with a single point of accountability rather than a fragmented team.

Ready to Make a Move?

If you want a clear picture of what you can afford and how the buying process will actually unfold in Miami-Dade, explore buyer resources at Labrada Realty. Alberto handles real estate, financing, and title in one place. One conversation gets you further than three separate calls.

Frequently Asked Questions

How much do I really need saved before buying my first home in Miami?

A: The answer depends on your loan type and whether you stack assistance programs. With an FHA loan at 3.5% down on a $480,000 home, your down payment is around $16,800. Add closing costs of roughly 2% to 4%, and you are looking at $25,000 to $36,000 out of pocket before assistance. Miami-Dade's County down payment assistance program can provide up to $35,000 as an interest-free deferred loan for qualifying buyers, and the Florida Hometown Heroes program adds up to $35,000 for eligible workers. A buyer who stacks these programs correctly can enter the market with significantly less cash than they assumed.

Is it better to buy a condo or a house as a first-time buyer in Miami?

A: Single-family homes in Miami-Dade have been more resilient in terms of value and easier to finance. Condos can offer a lower entry price point, but they come with HOA fees, building approval requirements for financing, and, increasingly, special assessment exposure related to reserve funding and structural integrity rules that took effect after 2021. Buildings older than 30 years that have not completed their milestone inspections face additional compliance costs. For a first-time buyer without a large cash reserve, a resale single-family home in West Kendall or Homestead often provides a more predictable ownership experience than a condo in a building with unresolved compliance issues.

What credit score do I need to qualify for a mortgage in Florida?

A: For a conventional loan, most lenders want a minimum score of 620, though a score of 700 or above will get you meaningfully better rates. FHA loans allow scores as low as 580 for the 3.5% down option, or as low as 500 with a 10% down payment. Florida's down payment assistance programs, including the County and Hometown Heroes options, generally require a minimum score of 640. If your score is between 580 and 640, you may still be able to buy, but your program options narrow and your rate will be higher. Twelve months of on-time payment history and reduced credit card balances relative to limits can move a score by 30 to 50 points more quickly than most buyers realize.

How do I protect myself when buying a new construction home in Miami?

A: Three steps make the biggest difference. First, bring your own buyer's agent. The builder's sales representative is not your advocate, regardless of how helpful they appear. Second, read the builder's contract carefully before signing. Florida new construction contracts typically favor the builder on delay provisions, specification changes, and dispute resolution. Third, commission an independent inspection at multiple stages of the build, not just the final walkthrough. Catching a framing issue before drywall is a minor fix. Catching the same issue at move-in is a legal dispute. Miami-Dade's permitting process is a compliance floor, not a guarantee of quality.

How long does it take to close on a home in Miami as a first-time buyer?

A: A standard financed transaction in Miami-Dade typically takes 30 to 45 days from accepted offer to closing. FHA loans can take slightly longer depending on the lender and whether the property requires appraisal conditions. Condo purchases add time if the building is not already on the lender's approved list, or if the association has a lengthy buyer approval process. New construction closings are driven by the builder's completion timeline and can shift by weeks without much notice. The fastest closings happen when the buyer is fully pre-approved before making an offer and when the team handling real estate, financing, and title is coordinated from day one.

Check out this article next