Most buyers assume a Miami Dade foreclosure comes pre-loaded with savings, list price below market, automatic upside, done. Buyers who treat it that way lose money, not because the math is impossible, but because they never ran it in the first place. Investors get hurt worse, since their entire return depends on a margin that often shrinks or disappears once rehab, insurance, and carrying costs get added back in. A foreclosure's listed price tells you almost nothing about what you'll actually spend to own it. Here's how to calculate whether the deal actually works, using real Miami-Dade numbers, before you put in an offer.

Why a Miami Dade Foreclosure Discount Isn't Automatically a Good Deal

A bank's listed price on a foreclosure is not the same thing as a discount. Miami houses in foreclosure carry a number set by a loss mitigation department, often based on an internal valuation model, sometimes adjusted because the asset has sat for a while, and almost never adjusted because anyone ran the same comps analysis a buyer would run.

Before assuming a listed price reflects a genuine discount, pull the actual final judgment amount on the case. The judgment amount is part of the public court record and originates from the Miami-Dade Clerk of Courts Civil Division downtown at 73 W Flagler Street, the office that processes the case file and eventually issues the certificate of title. Comparing the judgment amount, the listed price, and recent closed comps in the same zip code tells you whether you are looking at a real discount or a bank simply pricing to market.

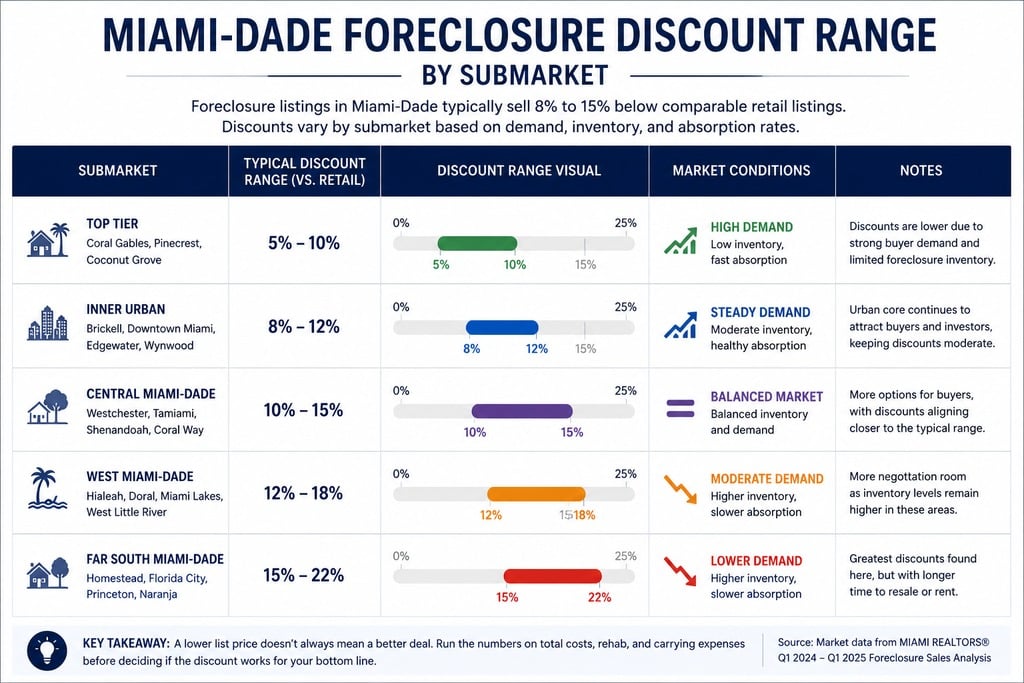

In Miami-Dade right now, foreclosure listings tend to trade somewhere in the range of 8 to 15 percent below comparable retail listings, though that spread compresses fast in high-demand submarkets and widens in areas with slower absorption. A property priced 20 percent under comps in a hot zip code usually means something is wrong with the property, not that you found a steal.

The guidance here is simple. Treat a Miami dade foreclosure listing as a starting point for research, not a number you react to. Pull comps. Pull the judgment amount. Then decide if there is a real spread worth pursuing.

The Full Cost Stack Most Buyers Forget to Calculate

Rehab is the cost everyone budgets for and still underestimates. Insurance is the cost almost nobody budgets for at all, and on older Miami-Dade housing stock, it can swing the entire deal.

A contractor walkthrough, not just an inspector's report, is what turns a guess into a number. Inspectors flag problems. Contractors price them. The gap between those two numbers is where a lot of projected margin quietly disappears.

Carrying costs are the other line item buyers forget. Every month between accepted offer and a tenant moving in, or a renovation finishing, costs money: loan payments if financed, insurance, utilities, property tax accrual, and in some cases an HOA assessment if the foreclosure happens to be in a condo or townhome community. Foreclosure homes in Miami dade sometimes sit vacant for a stretch before the bank lists them, which means deferred maintenance compounds the carrying cost problem before you even close.

One line item deserves its own mention because buyers consistently skip it: encumbrances that were not part of the original mortgage. A title company verifies whether anything else attaches to the property before you close, and that verification should be a hard line in your contingency budget, not an afterthought. Build a placeholder figure into your numbers for this, then let your title company replace the placeholder with a real figure before you remove contingencies. Review the hidden costs every buyer underestimates for a broader breakdown that applies with extra weight on a foreclosure.

Add rehab, insurance, carrying costs, and an encumbrance contingency together, and the real acquisition cost on miami dade foreclosure homes often runs 12 to 18 percent above the contract price. If your projected margin does not survive that math, the deal does not work, regardless of how good the discount looked on the listing page.

Running the Numbers: A Real Miami Dade Foreclosure Deal Example

A buyer I worked with was looking at a 3-bedroom, 2-bath REO in Hialeah, built in 1978, listed at $325,000. The home had been on the market 19 days, untouched, with a roof rated near the end of its useful life and a kitchen that had not been updated since the original construction.

We came in at $312,000 after the bank's first counter. A contractor walkthrough put rehab at $28,000: partial roof recoat, kitchen refresh, AC service, and flooring throughout. Carrying costs across a 45-day close and a 60-day renovation window, loan payments, insurance, utilities, added another $9,500.

Total all-in cost: $349,500. Recent comps on similar renovated 3-bedroom homes in the same zip code supported an after-repair value of $389,000, leaving roughly $39,500 in built-in margin before factoring in financing terms or holding the property as a rental.

Running it as a rental instead of a flip changes the math again. Market rent for a renovated 3-bedroom in that part of Hialeah was running close to $2,450 a month, or $29,400 a year gross. After insurance, quoted higher than average at $4,100 a year because of the roof's age and the property's wind mitigation rating, property tax near $5,200 at the new assessed value, and a maintenance reserve, net operating income landed around $17,750. Divided against the $349,500 total investment, that is a cap rate just over 5 percent.

Neither number is bad. Neither number is a windfall either. A disciplined Miami dade foreclosure homes buyer should expect numbers in this range once every cost gets counted, not the inflated spread that shows up when people only subtract list price from estimated resale value.

Where the Discount Is Real and Where It Disappears: Micro-Market Differences

The same foreclosure discount does not exist everywhere in Miami-Dade, and treating the county as one market is how investors misprice deals.

In high-demand submarkets like Brickell or Coral Gables, banks selling REO inventory know exactly what the property is worth. Multiple buyers are watching the same listing, offers come in within days, and the spread between list price and closing price narrows to almost nothing. Miami houses in foreclosure in these areas behave more like any other competitively priced listing than a distressed sale.

Move toward higher-inventory, slower-absorption areas, certain pockets of Hialeah, parts of West Kendall, sections of Miami Gardens, and the math changes. Fewer competing buyers, longer days on market before the bank adjusts price, and a real gap between what the bank is asking and what the property will eventually sell for once it is renovated.

Seasonal timing layers on top of this. Miami's traditional buying season runs roughly November through April, driven heavily by seasonal residents and international buyers who tend to purchase in cash and move quickly once they decide. A foreclosure listed in August in a slower submarket can sit through the entire off-season with minimal interest, then get multiple offers in January from buyers who were not even looking five months earlier. Knowing where you are in that calendar changes how aggressively you should negotiate and how much patience the seller actually has.

Investors building a portfolio sometimes look beyond single-family foreclosures entirely. Comparing property types for investment goals is worth doing before assuming a single-family flip or rental is automatically the right vehicle for the capital you have available.

The Variable That Wrecks Deal Math: Insurance and Financing Timelines

Every projection in the previous section assumes you can actually get insured at the number you modeled. Insurance is exactly where a lot of Miami-Dade foreclosure math falls apart.

Properties built before the 1990s, especially those with original roofs or aluminum wiring, often come back from insurance carriers with quotes well above what a buyer modeled at the offer stage. A quote that lands $1,500 to $2,000 higher than expected does not just hurt cash flow. It can push a loan's debt-to-income ratio out of range and stall financing entirely, sometimes after the appraisal and inspection period have already passed.

Get a real insurance quote, not an estimate, before your financing contingency expires. Waiting until the week of closing to find out the property is difficult to insure at a viable rate is how buyers lose earnest money on foreclosures that looked fine on paper.

If the foreclosure happens to be a condo, a different timeline risk shows up. Most associations require buyer approval before closing, and that process can take anywhere from a few days to several weeks depending on the building. A foreclosure with an aggressive bank-mandated closing deadline and a slow-moving condo board creates a collision that has killed more than one deal. HOA-heavy communities also carry their own cost variable: special assessments and reserve study findings that affect the building's master insurance policy, which in turn affects what unit owners pay. None of that shows up in a quick comps pull. It shows up when you actually request the association's financials and insurance certificate, which should happen before you are deep into a contract, not after.

Model your own financing scenarios, including a higher-than-expected insurance line, using the mortgage calculator before you submit an offer, not after the appraisal comes back.

When the Numbers Don't Work, and Who Should Be Running Them With You

Every Miami dade foreclosure deal has a point where the math stops working. Knowing that point before you submit an offer is what separates a calculated risk from a guess.

A few signals tell you to walk away regardless of how attractive the list price looks. If the rehab estimate from a licensed contractor exceeds 20 percent of the contract price, the margin almost never survives. If the insurance quote alone erases more than a third of your projected first-year cash flow, the deal is not actually cash flowing, it is breaking even with extra risk attached. If a title search turns up an encumbrance larger than your contingency line, renegotiate the price or pass. None of these are emotional decisions. They are math problems with clear answers once you have the real numbers in front of you.

The hard part is getting real numbers instead of estimates from three different people who do not talk to each other. A real estate agent estimates resale value. A lender estimates financing cost and timeline. A title company estimates what is actually attached to the property. When those three numbers come from three separate parties working independently, gaps show up, and gaps are where deals fall apart at the worst possible moment, usually a week before closing.

Running real estate, mortgage, and title under one roof closes that gap. Instead of reconciling three separate estimates after the fact, the acquisition cost, the financing terms, and the title picture get modeled together before an offer goes in, which is the only way the numbers in this article actually hold up once you are under contract on a real miami dade foreclosure.

[IMAGE: Alberto Labrada headshot. File: alberto-labrada-miami-dade-foreclosure-broker.jpg Alt: "Alberto Labrada, Miami Real Estate Broker, Labrada Realty"]

A Miami dade foreclosure can absolutely be a good deal. It is just never a good deal by default. The discount on the listing page is a starting assumption, not a guarantee, and the only way to know if it survives contact with rehab costs, insurance quotes, carrying costs, and whatever a title search turns up is to run the actual numbers before you are under contract, not after. Buyers who do that consistently find real margin in this market. Buyers who skip it find out the hard way that foreclosure homes in Miami dade are not automatically cheaper, just differently priced.

FAQ

Q: How do I tell if a Miami Dade foreclosure is actually priced below market value?

A: Compare three numbers before trusting any discount. Of the three, the easiest one buyers skip is checking the Miami-Dade Property Appraiser's property search for the home's assessed value history and prior sale price. If a property last sold for $410,000 in 2021 and is now listed at $325,000 with no major damage explaining the drop, that gap deserves more scrutiny, not less excitement. Pair that with recent closed comps in the same zip code, not active listings, and you get a realistic read on whether the number is a discount or a bank simply matching current conditions.

Q: What cap rate should I target on a Miami-Dade foreclosure rental property?

A: There is no single target that works countywide, since acquisition cost and rent both shift block by block. As a general benchmark, a renovated single-family foreclosure turned long-term rental in Miami-Dade should land somewhere between 5 and 7 percent on a cap rate basis once insurance, taxes, and a maintenance reserve are subtracted from gross rent. Properties closer to 5 percent usually sit in higher-demand areas where appreciation is doing more of the work than cash flow. Anything below 4 percent on a foreclosure specifically is a signal that the discount got eaten by rehab or financing costs before the rental math even started.

Q: How much rehab contingency should I budget into a Miami-Dade foreclosure deal?

A: A rehab contingency belongs on top of your contractor's number, not instead of it. On Miami-Dade foreclosures specifically, where deferred maintenance often includes roofing and HVAC systems pushed past their normal lifespan, add 15 to 20 percent on top of the contractor's bid as a contingency line, higher if the property has been vacant more than six months. Vacant homes in Miami's humidity develop problems that are not visible during a single walkthrough, including hidden mold behind drywall and AC systems that fail within weeks of being restarted after sitting idle. Building in that cushion protects your margin when something surfaces mid-renovation that nobody could see during due diligence.

Q: Why do insurance costs hit Miami-Dade foreclosure deals harder than retail purchases?

A: Foreclosure inventory in Miami-Dade skews older than the retail market on average, since these are often properties where an owner stopped maintaining the home well before the bank took it back. Homes over 20 years old typically require a four-point inspection for insurance purposes, covering roof, electrical, plumbing, and HVAC, and any one of those four systems in poor condition can push the property toward Citizens Property Insurance Corporation, the state-backed carrier of last resort, instead of a standard private carrier. Citizens coverage often costs more and comes with more restrictions than a comparable private policy on a retail purchase in similar condition, which is part of why insurance hits foreclosure math harder than a typical resale.

Q: What return on investment is realistic for a Miami-Dade foreclosure flip?

A: Realistic margins on a Miami-Dade foreclosure flip, after accounting for purchase price, rehab, carrying costs, and selling costs, typically land in the 8 to 12 percent range relative to total project cost on a well-executed deal. Numbers above that usually involve either an unusually motivated bank, a property other buyers overlooked for a fixable reason, or a renovation budget that came in lower than expected. Numbers below 5 percent are common too, and they are the ones that quietly turn into break-even projects once selling costs, which typically run 7 to 9 percent of sale price between commission, closing costs, and any concessions, get factored in at the back end.

If you have a Miami-Dade foreclosure you are trying to run real numbers on, whether it is a flip, a rental, or your own home, browse the current foreclosure inventory in Miami-Dade and reach out with the specific property. I will help you build the actual acquisition cost model before you submit an offer, not after.

Check out this article next