Florida has no state income tax, and a lot of sellers stretch that fact further than it goes. They assume it means selling a home here is close to a tax-free event. It isn't. Capital gains tax on home sale Florida transactions is a federal obligation, and it applies whether you sell in Homestead or Miami Gardens. The people who get hurt by this misunderstanding are usually sellers who owned a home for a long time, watched the value climb, and never ran the numbers before signing a listing agreement. By the time they see the closing statement, there's no room left to plan around it. This article walks through what you actually owe, what the exclusion protects, and how property taxes and insurance premiums change the real math around whether to sell now or hold.

Capital Gains Tax on Home Sale Florida: The Math Nobody Explains at Closing

Capital gains tax is calculated on your profit, not your sale price. Profit means the sale price minus your cost basis minus qualifying selling costs. Your cost basis starts with what you originally paid, then adds documented capital improvements: a new roof, a kitchen remodel, an addition. Routine repairs and maintenance don't count.

Here's the part that trips people up. A home bought in 2005 for $280,000 and sold today for $650,000 doesn't owe tax on $650,000. It owes tax, if any, on the gain above basis and above the applicable exclusion. Federal long-term capital gains rates run 0%, 15%, or 20% depending on your total taxable income for the year, and a Net Investment Income Tax of 3.8% can apply above certain income thresholds. Florida adds nothing on top of that federal number, which is the one part of the "no state tax" claim that's actually true.

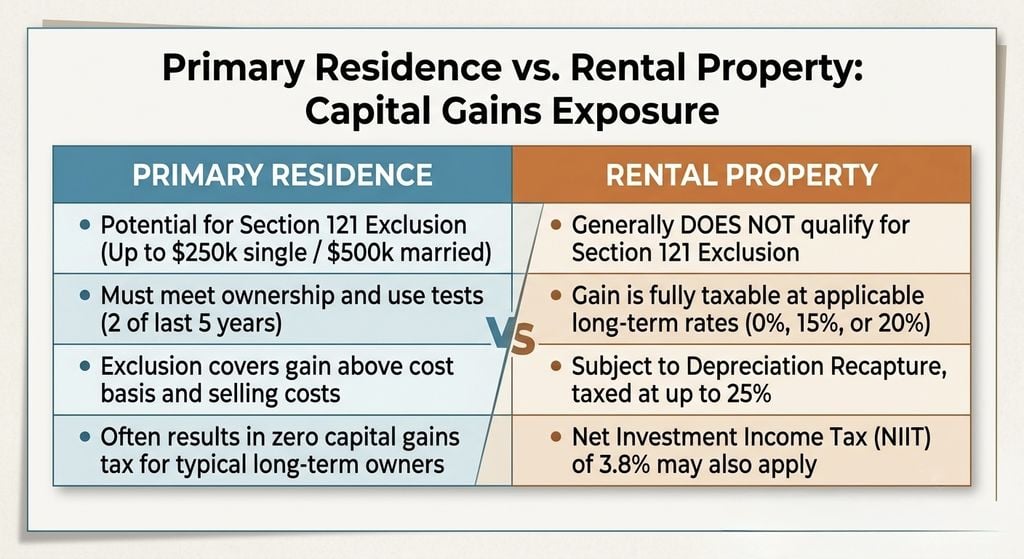

The $250,000 / $500,000 Exclusion and Where Sellers Miscalculate It

Section 121 of the tax code lets a single filer exclude up to $250,000 of gain, and a married couple filing jointly exclude up to $500,000, on the sale of a primary residence. To qualify, you generally need to have owned and lived in the home as your primary residence for at least 2 of the last 5 years before the sale.

Sellers miscalculate this in three common ways:

- They forget the exclusion is per-sale, not automatic. You still have to calculate your actual gain to know if it falls under the cap.

- They can't document capital improvements because they didn't keep receipts, which inflates their taxable gain unnecessarily.

- They assume a second home or a rental property qualifies for the same exclusion, when it generally does not without meeting the residency test.

A seller who owned a Kendall home for 12 years, lived in it the entire time, and nets a $310,000 gain as a married couple owes nothing in capital gains tax. The same gain on a rental property they never lived in could be fully taxable, plus subject to depreciation recapture. The difference between those two outcomes is documentation and timing, not luck.

Foreign Sellers Face a Different Rule Entirely

Miami-Dade has a large share of foreign national owners, and the capital gains conversation changes completely for them. Under FIRPTA, the Foreign Investment in Real Property Tax Act, a buyer's closing agent generally must withhold 15% of the gross sale price, not the profit, and send it to the IRS at closing when the seller is a foreign person. A foreign seller can apply for a withholding certificate before closing to reduce that amount to something closer to their actual tax liability, but the application takes weeks, so timing matters.

I've seen deals almost fall apart at the closing table because a foreign seller assumed the withholding worked like the residency exclusion available to U.S. taxpayers. It doesn't. A Brickell condo owner who is a nonresident alien can owe FIRPTA withholding on the full sale price even if their actual gain is modest, and getting that money back requires filing a U.S. tax return the following year. Planning for this before listing, not at the closing table, is the difference between a smooth wire transfer and a seller scrambling for cash to close a simultaneous purchase.

How Much Are Property Taxes in Miami: The Number That Resets When You Sell

How much are property taxes in Miami depends less on your home's value than on how long you've owned it. Miami-Dade combined millage rates, which stack county, city, school board, and special district levies, typically run somewhere between 18 and 21 mills depending on the municipality. The City of Miami's combined rate sits close to 20 mills, meaning roughly $20 in tax for every $1,000 of taxable value.

The Save Our Homes cap is why two nearly identical homes on the same street can carry completely different tax bills. For homesteaded properties, assessed value increases are capped at 3% annually or the change in the Consumer Price Index, whichever is lower, no matter how fast market value rises. An owner who bought 15 years ago and never sold can have an assessed value tens of thousands of dollars below market value. The 2026 homestead exemption sits at $51,411, which further reduces the taxable base for qualifying owners.

Here's what sellers miss: that gap disappears the moment you sell. The buyer's assessed value resets to current market value in the year following the sale, and their tax bill can jump immediately, sometimes doubling what the seller was paying. This matters for negotiations, because a savvy buyer's lender will calculate their monthly payment using the higher, post-sale tax figure, not your old bill, which affects what they can actually afford to offer.

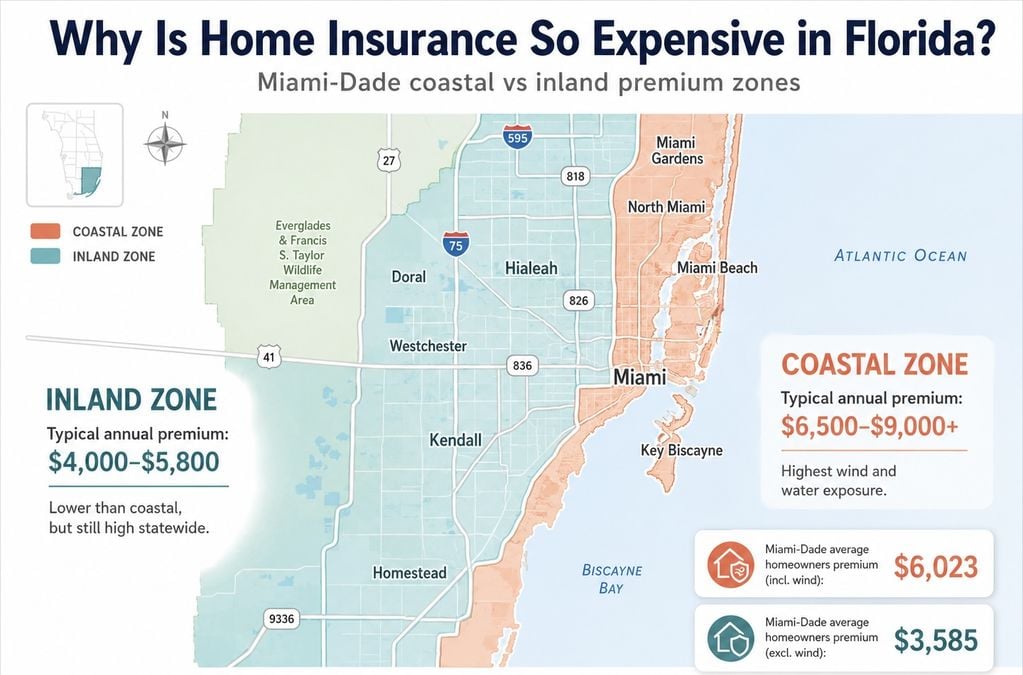

Why Is Home Insurance So Expensive in Florida (And Why It's Now Stalling Closings)

Why is home insurance so expensive in Florida comes down to three compounding factors: hurricane exposure, rebuilding costs, and, until recently, a wave of litigation that inflated insurer losses statewide. Florida's average annual premium reached roughly $8,292 in 2025, an 18% jump from the year before, and industry forecasts put 2026 close to $8,458. South Florida coastal counties, including Miami-Dade, sit at the higher end of that range because of storm exposure and older housing stock.

There's a genuine bright spot. Legislative reforms passed in 2022 and 2023 reduced the lawsuit activity that had been driving losses, and Citizens Property Insurance, the state's insurer of last resort, cut rates by an average of 8.7% at 2026 renewals. Several private carriers have filed rate reductions and new insurers have re-entered the state. Premiums are stabilizing, not falling fast, but the direction has changed.

What this means for a sale in progress: insurance underwriting now directly affects closing timelines. Roof age past 15 to 20 years, an outdated 4-point inspection, or a lapse in wind-mitigation credits can delay or derail a buyer's ability to bind a policy, which delays their loan approval. I've watched closings slip two to three weeks because a seller assumed their existing policy would simply transfer, when in reality the buyer's lender required a fresh quote before clearing to close.

Condos and HOAs: A Different Tax and Insurance Equation

Everything above changes shape once you're selling a condo or a home inside an HOA-heavy community, and this is where a lot of Miami-Dade sellers get caught off guard. Condo buildings carry their own master insurance policy, and after several years of rising reinsurance costs, associations across Brickell, Miami Beach, and Coconut Grove have passed special assessments running from a few thousand dollars to well over $50,000 per unit to cover insurance gaps and mandatory structural inspections under Florida's post-Surfside reserve requirements. A pending special assessment can delay a buyer's mortgage approval by weeks while the lender confirms the building's reserve funding status, which is a different problem than anything a single-family seller deals with.

Single-family homes in non-HOA communities skip that layer of approval risk entirely, but they carry the full insurance and roof-age underwriting burden alone, without a master policy spreading the cost across dozens of units. This is part of why how much are property taxes in Miami and how much insurance costs in Miami can vary so widely between a condo in Edgewater and a single-family home in the same tax bracket in West Kendall. Sellers in HOA communities should also confirm the association's estoppel and approval timeline before accepting an offer, since some boards take 30 days or longer to approve a buyer, which affects your closing date regardless of financing.

A Real Miami-Dade Seller's Math for Capital Gains Tax on Home Sale Florida

Take a couple who bought a home in Palmetto Bay in 2011 for $340,000. Over the years they added a new roof ($22,000), a kitchen renovation ($38,000), and impact windows ($16,000), bringing their adjusted cost basis to $416,000. They sell in 2026 for $780,000, with $47,000 in selling costs (commission, title, transfer taxes).

Their gain calculation: $780,000 sale price, minus $47,000 in selling costs, minus $416,000 adjusted basis, equals $317,000 in gain. As a married couple filing jointly who lived in the home the full period, their $500,000 exclusion fully covers that gain. Federal capital gains tax owed: zero.

Now change one variable. If this had been a rental property they never lived in, that same $317,000 gain would be fully taxable at their applicable long-term rate, plus depreciation recapture taxed at up to 25%. The difference between those two outcomes, potentially tens of thousands of dollars, comes down entirely to whether they met the 2-of-5-year residency test and kept their improvement receipts.

The Mistake That Costs Sellers the Most: Treating These Costs as Separate Decisions

Most sellers evaluate capital gains tax, property tax exposure, and insurance premiums as three unrelated line items. They aren't. They're one connected decision about whether to sell now, hold, or convert the property to a rental.

Consider an owner sitting on a low Save Our Homes assessment who is also facing a rising insurance premium on an aging roof, the exact combination that explains why is home insurance so expensive in Florida for owners who have delayed roof replacement. Holding the property keeps the low tax bill but locks in the higher insurance cost every year until the roof is replaced. Selling resets the buyer's tax bill higher but transfers the insurance and roof-age problem to someone else's underwriting file. Converting to a rental preserves neither the primary-residence exclusion timeline nor the homestead exemption, and it starts a clock on the 2-of-5-year rule that, once it expires, permanently changes the tax exposure on a future sale.

This is where running the actual numbers before listing matters more than any staging decision or listing price strategy. A seller who understands their adjusted basis, their exclusion eligibility, their buyer's likely post-sale tax bill, and current insurance underwriting standards walks into a negotiation with leverage. A seller who doesn't finds out what they owe after the fact, when there's nothing left to plan around. If you're weighing whether now is the right time to sell in Miami-Dade, our guide on selling your house in Miami walks through the timing questions that pair with this math, and our breakdown of home improvements that add value before you list is worth reading before you finalize your cost basis records.

For a full look at which renovations actually move your basis and your resale number, see Top Home Improvements in Miami: ROI, Financing, and the IRS.

According to the IRS Topic No. 701, sale of a home rules are detailed directly from the source, and the Florida Department of Revenue publishes the county-by-county millage data referenced above. For insurance-specific guidance, the Florida Office of Insurance Regulation tracks current rate filings and Citizens Property Insurance eligibility rules.

FAQ

Q: Do I have to pay capital gains tax when I sell my house in Florida?

A: Only on the portion of your gain above your cost basis and above your exclusion. If you're single, the first $250,000 of gain is excluded; married couples filing jointly exclude up to $500,000, provided you owned and lived in the home as your primary residence for at least 2 of the last 5 years. Most long-term Miami-Dade owners who lived in their homes fall entirely within this exclusion and owe nothing federally. Investment properties and homes owned less than 2 years are far more likely to generate an actual tax bill.

Q: How much are property taxes in Miami-Dade compared to other Florida counties?

A: Miami-Dade consistently ranks among Florida's highest-tax counties in raw dollar terms, driven by combined millage rates near 18 to 21 mills and high underlying property values. A homesteaded owner benefits from the Save Our Homes cap, limiting assessment growth to 3% annually or the CPI, whichever is lower, which can keep a longtime owner's bill far below a recent buyer's on the identical street. Non-homesteaded and investment properties don't get this protection and are reassessed at market value every year.

Q: Why is home insurance so expensive in Florida right now?

A: Hurricane exposure, high rebuilding costs, and years of litigation-driven insurer losses pushed Florida's average premium to roughly $8,292 in 2025, nearly three times the national average. The good news is that 2022 and 2023 legal reforms have slowed the growth, and Citizens Property Insurance cut rates by 8.7% for 2026 renewals as several private carriers have filed decreases too. Coastal Miami-Dade properties still sit at the higher end of the state range because of storm risk and older housing stock.

Q: Can I avoid capital gains tax if the home was a rental or second home?

A: The primary Section 121 exclusion generally requires the home to have been your main residence for 2 of the last 5 years, so a straight rental or vacation property usually doesn't qualify for the full exclusion. Some owners convert a rental to a primary residence and later qualify for a partial exclusion, but IRS rules prorate the excluded amount based on how the property was used during ownership. Depreciation recapture also applies separately to rental properties and is taxed differently than the standard gain.

Q: Does my low property tax bill disappear the moment I sell?

A: Yes, effectively. The Save Our Homes cap and homestead exemption are tied to the owner and the property's use as their primary residence, not to the home itself. Once you sell, the buyer's assessed value resets to current market value the following tax year, and their bill can be significantly higher than what you were paying. Buyers should always calculate their real, post-sale property tax before finalizing their offer, and sellers should expect this to come up in negotiations.

Q: Should I sell now or convert my home to a rental to avoid the capital gains hit?

A: It depends on your timeline. Converting to a rental starts eroding your eligibility for the 2-of-5-year primary residence exclusion, and once that window closes, a future sale could be fully taxable. It also forfeits your homestead exemption and Save Our Homes protection going forward, which usually raises your annual property tax immediately. For most owner-occupants planning to sell within a few years, selling while still homesteaded and within the residency window preserves more value than converting to a rental first.

If you want a real number on what you'd net after capital gains tax, property tax proration, and today's insurance market, not a rough guess, get a free home valuation and we'll walk through the actual math together before you decide whether to sell, hold, or wait.

Disclaimer:

This article is for general informational purposes only and does not constitute tax, legal, financial, or accounting advice. Capital gains tax rules, exclusion amounts, millage rates, homestead exemption values, and insurance premiums change over time and vary by individual circumstances. Nothing in this article should be relied on as a substitute for advice from a licensed CPA, tax attorney, or financial advisor regarding your specific situation. Alberto Labrada is a licensed Florida real estate broker and is not a CPA or tax attorney. Property tax figures, insurance data, and other numbers cited here reflect publicly available sources as of the date noted above and may have changed. Consult the Miami-Dade Property Appraiser, the Florida Department of Revenue, a qualified tax professional, or a licensed insurance agent before making any decision based on this information.

Check out this article next