Most people searching Miami Dade rentals assume a condo works the same way a rental house does. Sign a lease, move in, done. Condos and apartments in Miami-Dade run on a completely different set of rules, and renters who skip that part end up blindsided by rental caps, association approval delays, or a building that will not let them lease at all. Buyers face a mirror version of the same problem. The HOA fee that looked manageable on paper turns into a monthly number that changes whether owning actually beats renting. This guide walks through what condos and apartments across the county actually cost to rent right now, what buying the same unit costs once HOA fees and insurance enter the picture, and where the real math lands when you run both numbers side by side.

What "Miami Dade Rentals" Means When You're Weighing a Condo or Apartment

Search Miami Dade rentals today and the results blend three different products together: standalone apartments in large managed communities, individually owned condos leased out by their owners, and co-op style units that still show up occasionally in older Miami Beach buildings. Each one plays by different rules.

Managed apartment communities, common in Doral, Kendall, and parts of Westchester, operate like a business. Applications move fast, pricing is set by revenue management software, and rental caps do not apply because the entire building is designed for renters.

Individually owned condos are a different animal. An owner leasing a unit in a Brickell or Edgewater tower is bound by whatever the condo association allows, and associations in Miami-Dade increasingly cap the percentage of units that can be leased at once, sometimes as low as 10 to 20 percent of the building. If that cap is full, the owner cannot legally rent the unit no matter how good the price looks online.

This distinction matters just as much on the buying side. A buyer comparing renting v buying in one of these towers needs to know the association's rental policy before making an offer, because a restrictive rental policy affects resale value and financing in ways a house never does.

Miami Dade Rentals by Area: What Condos and Apartments Actually Cost Right Now

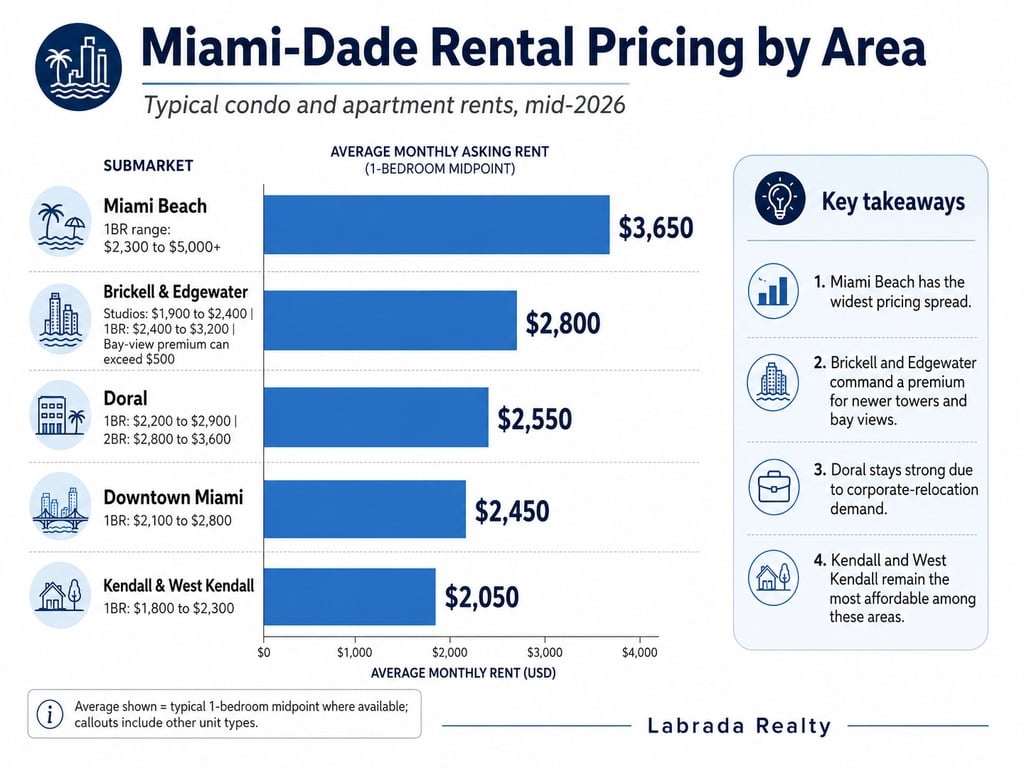

Pricing for Miami Dade rental properties in the condo and apartment segment varies more by building than by zip code, but here is a realistic range by area as of mid-2026.

- Brickell and Edgewater: Studios run $1,900 to $2,400. One-bedrooms run $2,400 to $3,200. Buildings along Biscayne Blvd and South Miami Ave command a premium for bay views, sometimes $500 or more above an identical unit facing inland.

- Downtown Miami: Slightly below Brickell for comparable square footage. One-bedrooms typically run $2,100 to $2,800, with older buildings pricing well below newer towers that carry heavier amenity packages.

- Doral: Apartment communities dominate here. Expect $2,200 to $2,900 for a one-bedroom and $2,800 to $3,600 for a two-bedroom, with strong demand tied to corporate relocation.

- Kendall and West Kendall: The most affordable condo and apartment inventory in the county for renters who want proximity to good schools without Coral Gables pricing. One-bedrooms run $1,800 to $2,300.

- Miami Beach: The widest range in the county. A basic one-bedroom off the beach can run $2,300, while an oceanfront unit in a full-service building can clear $5,000.

This pattern holds true across most Miami Dade rental properties: a condo with a low HOA fee usually rents for more, because the owner is pricing in a lower carrying cost and can afford to hold firm on rent. A condo with a high HOA fee often prices the rent lower, because the owner needs the unit occupied to cover the fee. Renters chasing the lowest sticker price sometimes end up in the building with the highest ongoing costs, which matters later if they want to buy in that same building.

Demand for condo and apartment rentals in Miami-Dade also follows a seasonal curve tied to when snowbirds and international residents arrive. Inventory tightens from January through April, when seasonal residents and relocating families push demand up and asking rents firm across nearly every price tier. Renters who search in May through August typically find more room to negotiate, since owners carrying vacant units during slower months are more willing to come down on price or offer a rent credit for a longer lease term.

What Buying That Same Unit Actually Costs

Renters comparing the sticker price of a mortgage payment to their rent are usually comparing the wrong numbers. A condo's real monthly cost includes the HOA fee, and in Miami-Dade that fee has moved sharply since the state's structural reserve requirements took effect following the Surfside collapse. Buildings over 30 years old are now required to fund full reserve studies and collect enough in reserves to cover major structural repairs, and many associations raised fees or issued special assessments to comply.

A unit with a $450 monthly HOA fee in 2022 might carry a $650 to $800 fee today if the building underwent a reserve study and adjusted its budget. Some owners in older Miami Beach and Downtown buildings have faced special assessments running into five figures per unit, billed as a lump sum or a payment plan on top of the regular fee.

Insurance compounds this. Condo master policies in Miami-Dade have climbed sharply over the past several years, and that cost gets passed through the HOA fee or, in some buildings, billed as a separate insurance assessment. Lenders reviewing a loan application now scrutinize a building's insurance coverage and reserve funding as closely as they scrutinize the borrower, and a building that fails to meet reserve requirements can become unwarrantable, meaning conventional financing falls apart entirely regardless of the buyer's credit. Foreign buyers, who make up a significant share of Miami-Dade condo purchases, often pay cash specifically to sidestep this issue altogether, which is one reason an all-cash offer on a non-warrantable building can still close while a financed offer on the same building falls through.

None of this shows up in a simple mortgage calculator comparison. A buyer needs the building's most recent budget, reserve study, and insurance declarations before running real numbers against a rental comparison.

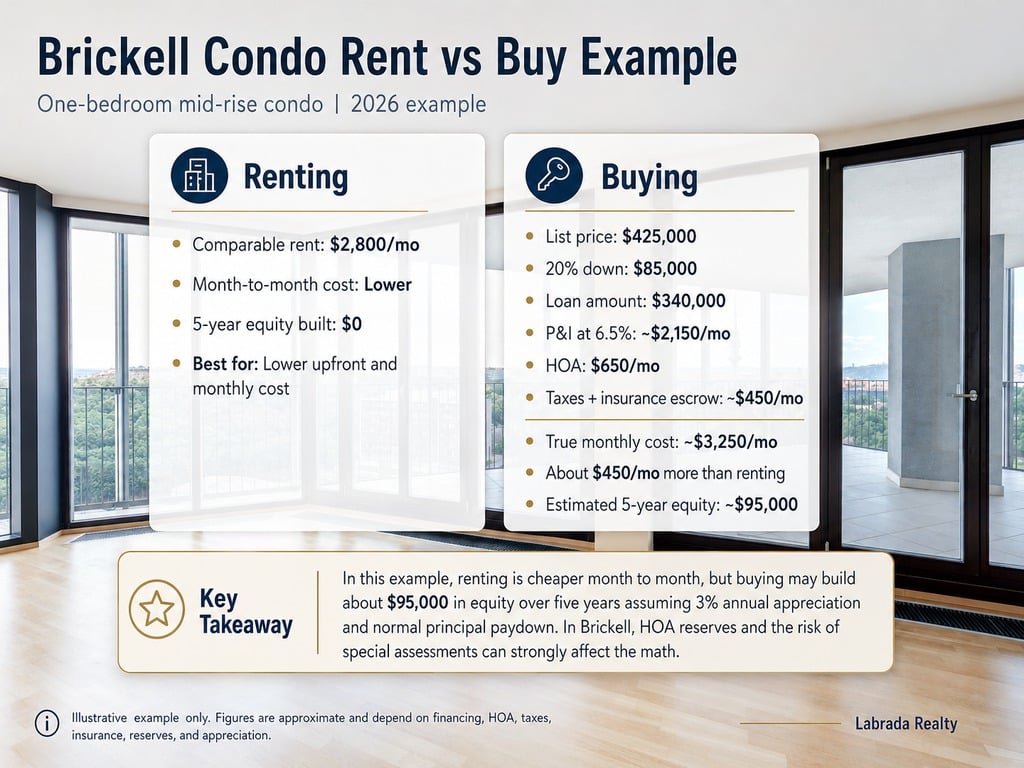

The Real Math: A Brickell Condo Example

Take a one-bedroom unit in a mid-rise Brickell building, listed at $425,000. Renting a comparable unit in the same building currently runs $2,800 a month.

Buying with 20 percent down, a $340,000 loan at a 6.5 percent rate runs approximately $2,150 a month in principal and interest. Add a $650 HOA fee and roughly $450 a month in property tax and insurance escrow, and the real monthly cost lands closer to $3,250, about $450 more than renting the identical layout.

The buyer's break-even shows up in equity, not monthly cash flow. Over five years, assuming modest 3 percent annual appreciation and normal principal paydown, that buyer builds roughly $95,000 in equity while the renter's $2,800 a month builds none. But that math only works if the building's reserves stay funded and no special assessment hits during the hold period, which is exactly why the reserve study and insurance declarations matter more in this market than almost anywhere else in Florida.

A renter who assumed the mortgage payment alone would beat rent would have walked away from this building. Once HOA and escrow entered the picture, renting was cheaper month to month, and only made sense to abandon once the five-year equity picture was on the table.

Condo Association Rules That Change the Decision

Rental caps are the single biggest surprise for people who assume renting v buying in a condo works like it does with a house. Many Brickell and Edgewater associations cap leased units at 10 to 25 percent of the building, and once that cap is reached, no additional owner can legally lease their unit until another lease ends and a slot opens up. Some buildings maintain a waitlist for lease approval that runs several months.

Approval timelines add another layer. Even in buildings without a hard cap, association board approval for a new tenant commonly takes 10 to 21 days, sometimes longer if the board only meets monthly. A renter under time pressure to move can lose a unit they already applied for simply because the board did not convene in time.

Buyers face the warrantability issue directly. Fannie Mae and Freddie Mac guidelines require a building to meet specific reserve funding, insurance, and owner-occupancy thresholds to qualify for conventional financing. A building with too many rental units, insufficient reserves, or unresolved structural issues becomes non-warrantable, which pushes buyers into higher-rate portfolio loans or cash purchases only. This is precisely where having a broker who also holds a mortgage license changes the outcome. Alberto Labrada checks the warrantability question against the building's condo questionnaire before an offer goes in, not after a buyer has already fallen in love with a unit and the loan falls apart during underwriting.

The Mistake Renters and Buyers Both Make Comparing Condos in Miami-Dade

The most common mistake in Miami Dade rental properties on the rental side is signing a lease without confirming the building's rental cap status first. A renter who signs, pays a deposit, and then discovers the association will not approve the lease because the cap is full loses time, the deposit in some cases, and has to restart the search from zero, often with a moving deadline now days away instead of weeks.

The most common mistake on the buying side is running the numbers against the listed HOA fee without checking whether a special assessment is pending or a reserve study increase is scheduled. Buyers who skip this step can close on a unit only to receive an assessment notice a few months later that adds hundreds of dollars a month to a payment they had already budgeted tightly. The building's condo questionnaire and the last two board meeting minutes reveal this information reliably, and both are available before closing, not after.

The math on Miami Dade rentals never comes down to comparing a lease payment to a mortgage payment. It comes down to knowing the building, the association's rules, and whether the numbers you were sold match the numbers the reserve study and insurance declarations actually show. Renters who check the rental cap before signing and buyers who check the reserve study before making an offer end up with the outcome they expected. Everyone else finds out the hard way.

If you are searching for a house instead of a condo, Miami-Dade houses for rent follow a different set of rules entirely, worth reading before you commit to one property type over the other. And if you want the broader financial case for renting versus owning a single-family home in Miami, is it better to rent or buy a house in Miami covers that comparison directly. For a deeper look at the Brickell condo market specifically, condos in Miami Brickell breaks down the investor angle building by building.

For official guidance on landlord-tenant law in Florida, Florida Statute 83 covers the legal framework governing residential leases. For condo-specific reserve requirements enacted after the Surfside collapse, Miami-Dade County's building recertification program outlines what associations must comply with. For general guidance on mortgage qualification and financing, the Consumer Financial Protection Bureau's mortgage resources are a reliable, plain-English reference.

FAQ

Q: Is it cheaper to rent or buy a condo in Miami-Dade right now?

A: In most Brickell and Edgewater buildings, renting currently costs less month to month than buying the same unit once the HOA fee, insurance escrow, and property tax are added to the mortgage payment. A $425,000 one-bedroom that rents for $2,800 a month typically costs closer to $3,250 a month to own with 20 percent down at current rates. The gap closes over time through equity buildup and rising rents, but the immediate cash flow advantage usually favors renting unless the buyer plans to stay five or more years.

Q: How do HOA rental restrictions affect Miami Dade rental properties?

A: Associations across Miami-Dade increasingly limit the share of units that can be leased at one time, often to 10 to 25 percent of the building. Once that cap fills, owners cannot legally lease their unit until another lease ends, and some buildings maintain a formal waitlist for the next available slot. Renters searching Miami Dade rental properties in a capped building should confirm availability with the association directly, since listing sites rarely reflect real-time cap status and a lease signed before confirming can fall apart during board approval.

Q: What's the difference between renting a condo and renting an apartment in Miami-Dade?

A: A rental apartment typically sits inside a professionally managed community built specifically for renters, with standardized pricing and no association approval process beyond a background and credit check. A condo rental means leasing from an individual owner inside a building where most units are owner-occupied, which brings association rules, board approval timelines of 10 to 21 days, and sometimes a rental cap into the process. Apartments generally move faster to lease. Condos can offer better locations and finishes but require more patience and paperwork before move-in.

Q: How does condo insurance affect the decision to rent vs. buy?

A: Rising master insurance premiums in Miami-Dade get passed through to owners as part of the HOA fee or as a separate assessment, and lenders now review a building's insurance coverage closely before approving a conventional loan. A building with insufficient coverage or an expired policy can become unwarrantable, cutting off standard financing entirely. Renters do not absorb this cost directly, but a spike in insurance-driven HOA fees eventually shows up in higher asking rents as owners try to offset their own rising carrying costs.

Q: Can I still rent a unit if the building's rental cap is already full?

A: Generally not, at least not legally through the association's approval process. Some owners in capped buildings attempt short-term workarounds like unregistered subleases, which put both the tenant and the owner at risk of an association fine or eviction action. The safer path is asking the association directly for the current leased-unit percentage and, if the cap is full, getting on the waitlist or searching buildings nearby with more room. Buildings in Doral and West Kendall tend to carry less restrictive rental policies than luxury towers in Brickell and Miami Beach.

If you are trying to figure out whether a specific condo or apartment actually pencils out to buy instead of rent, run the numbers on our mortgage calculator with the building's real HOA fee and insurance costs factored in, then reach out and we can pull the reserve study and rental cap status together before you make a decision.

Check out this article next